THESES OF DOCTORAL (PhD) DISSERTATION

UNIVERSITY OF KAPOSVÁR

FACULTY OF ECONOMIC SCIENCE

DEPARTMENT OF FINANCE AND ACCOUNTING

Leader of the doctoral school:

Prof. Dr. KEREKES SÁNDOR DSc professor

Thesis advisor:

DR. WICKERT IRÉN PhD

FURTHER DEVELOPMENT OF PLANNING METHODS OF LOCAL GOVERNMENTS

A SHIFT TOWARDS A STRATEGY-ORIENTED MANAGEMENT APPROACH

Prepared by:

SISA KRISZTINA A.

KAPOSVÁR 2014.

2

TABLE OF CONTENT

1. Research history, research objectives ... 3

1.1. Research history ... 3

1.2. Research objectives ... 4

2. Material and method ... 7

3. Results... 10

3.1. Characteristics of long term – strategic – planning ... 10

3.2. Short term – annual – planning ... 18

3.3. Role of the size of the government and the state of development of planning processes and methods ... 22

3.4. Factors of receptivity towards innovation ... 26

3.5. The future of planning ... 27

4. Consequences ... 30

5. New and recent research findings ... 32

6. Proposals (theoretical and practical application ... 35

7. Scientific publications written in the topic of the

dissertation; informative publications ... 40

3

1. RESEARCH HISTORY, RESEARCH OBJECTIVES

1.1. Research history

In the past years, a number of domestic studies1 have been elaborated on the economic and financial situation of self-governments, and they all lead to the conclusion that experts urge the execution of reform measures affecting the administration of self-governments, the financing of the implementation of duties, and planning.

It is in the interest of the national economy to enable the establishment of a planning system allowing for the most accurate determination of the volume of public and generated funds, which finance the transparency of the performance of their public services, duties and the quality of the administration. The aspiration and commitment of the “state” – as the highest level – towards the reforming of the system of self-governments is well demonstrated by the Hungarian National Reform Program of 2013, and by the objectives of the Public Administration and Development Program of Magyary Zoltán affecting the reform measure MP12.0 on self-governments.

The reform is also urged by an international pressure, since Directive 85/2011 of the EU orders the development of the budgetary framework of member states. The Directive had an impact on the development-related obligations of all sub-sectors of public finances, and it had to be adapted into national legislation by the 31st December 2013. As the first step of the implementation of national intentions and international expectations, the

“new” act CXCV. of 2011 on public finances, and act CLXXXIX. of 2011 on the local self-governments of Hungary were constructed – amongst others.

1 For details, see the publications of ÁSZ (2007), Csapodi (2009), Lóránt (2010), Pálné (2008), Vígvári (2008, 2009, 2011), Báger - Vígvári (2007).

4

Furthermore, on account of the new regulations on accounting2 effective as of 2014, the budgetary accounting information system will also be reformed, by the extension of a result-oriented accounting approach to the budgetary sector, and by the application of a transparent and unified economic and functional classification (COFOG).

According to my hypothesis – which is based on the purposeful and careful application of the instruments of the NPM (New Public Management) and the “neo-weberian” principles – the corporate planning methods successfully applied by the private sector and a parallel approach enable the opportunity for self-governments to operate the planning processes and planning systems in a more efficient manner, and these also allow for the optimization of the conditions and circumstances of the administration, and for the improvement of the quality of public services. The justification for the application of management methods at self-governments is also substantiated by both the Magyary Zoltán Development Program designed to modernize the Directive and the administration, and the National Reform Program.

1.2. Research objectives

When appointing the basic objectives of my research I have focused on the process of planning on the level of domestic self-governments, and also on methodological issues.

There are two main objectives regarding my research:

Based on existing literature and the results of the empiric research I aspire to present a complex picture about the process of planning systems at the self-government of settlements, and about planning methods which are already or could be applied in practice, and after the

2 4/2013(I.11) Government regulation on the accounting of public finances

5

summarizing of results I will also perform a “SWOT” analysis on the planning system itself.

The other objective of my research is to explore the areas to be renewed of the planning system of self-governments from the aspect of methodology, and also to determine the key factors of innovation.

Throughout the improvement process, I will consider the corporate planning methods of the business sector as the basis, since I believe that the majority of methods could be successfully adapted by the public sector as well. I aspire to place special attention on the reconsideration of the notion of strategic-tactical planning, on the strengthening of the strategic role of the economic program, and in terms of short-term planning, also on the fields of program planning and cost-accounting budget planning. The introduction of a result-oriented accounting approach indicates favourable changes within the sector from the aspect of my research proposals, establishing the information and methodological base for the elaboration of planning methods built on financial and accounting data. I believe that the accounting information system of self-governments has become suitable for the elaboration of a management accounting sub-system. My proposals on planning and in relation to management accounting are drawn up along the rules of cost- accounting.

In order to be able to realize my research objectives, I attempt to prove the following hypotheses:

1. Self-governments of settlements do prepare long term plans – typically in order to complete legal obligations -, however they do not execute actual formalized and complex strategic planning processes. An economic program cannot be considered as a strategic plan document and management instrument, which supports balanced operation and administration in the long run.

6

2. The application of modern program budget planning techniques is on a low level at self-governments in Hungary. I assume that in case of self- governments of settlements, its usage would be reasonable in case of decisive, well programmable functions.

3. Budget planning methods must be differentiated, considering the activity, the nature and content of the public service duty, and the programmability of emerging costs.

4. Regarding the state of development of planning systems within the Hungarian self-government sector, self-governments of settlements can be described with the same characteristics as “a mass”, irrespective to their size. From the point of view of the characteristics of the planning system and the development of its methods, there is no need for segmentation by size.

5. Based on my preliminary hypotheses – which have been built on the research results of Mohr, 1969. and Berry, 1994. – self-governments in Hungary consider the necessity of the innovation of their planning system to various extents, depending on the financial situation, their openness, regional position and the approach of the management.

7

2. MATERIAL AND METHOD

In order to be able to complete my research objectives and to confirm my preliminary hypotheses, I have conducted both primary and secondary research activities as well.

The secondary research has been carried out by processing national and international literature and relevant legislations regarding the “traditional”

and “management” approach of planning, its processes and methods. The procession of literature enables the opportunity to harmonize and clarify definitions, and also to compare and confront theories and practical experiences regarding the methods and instruments of planning. I was motivated to study national and international research results in order to be able to assess the typical characteristics of planning occurring in the sector of self-governments, which then served as a basis for the drafting of my proposals regarding the further development of the planning system.

The results of the secondary research activities must support the process, methods and results of the empiric research to a great extent, which constitutes the second major part of my study. I have conducted my primary research with the execution of an empirical research based on previously planned qualitative and quantitative data collection. Data collection was implemented by the conduction of interviews, and a questionnaire survey, which is considered to be the most popular primary information gathering technique. The representativity of the sample was ensured by an appropriate sample size, and also by the method of random sampling, from a population consisting of the self-government of settlements. After the planning of the sampling method, I attempted to distribute the self-administrative questionnaires to respondents through various channels.

8

I contacted a number of associations of self-governments, including TÖOSZ (national association of the self-government of settlements), MJVSZ (association of towns with county right) and BÖSZ (association of Budapest self-governments).

The filling out and collection of questionnaires has been quite difficult, therefore I have involved college students in the research, and I also personally contacted local governments, asking them to fill out the questionnaire. The collection of data lasted more than one month, since questionnaires had to be sent out repeatedly, in order to increase their number, and thus of the sample. There were a total number of 600 questionnaires sent out, and I have managed to make use of 64 valid replies for this part of my empirical research.

Throughout the primary data collection, my purpose was to explore the planning process and applied methods at self-governments and to provide a thorough evaluation, from the point of view of the self-governments of capital districts, towns with county rights, towns and settlements. The SPSS statistical analysis program was applied during the operative part of the empirical research. The data extracted from the questionnaires were typically qualitative data. On account of the observations made by quantitative data, measurements were conducted on a nominal and ordinal scale. A great variety of statistical analysis methods are available now for analysing a database. The actual application of these various statistical analysis methods was complicated by the fact that the data to be analysed were mainly quantitative data measureable on a nominal and ordinal scale.

As a consequence, descriptive statistical analysis prevail throughout the research, however I also attempt to explore causalities with the help of statistical independence analysis.

9

The population of the sample indicates a small sample, therefore when selecting further methods, I preferred those statistical methods which are better applicable on a small sample. Considering these criteria and characteristics, the available data was analysed with an independence analysis implemented by Chi-squared tests, two-sample T-tests, variance analysis and cluster analysis.

10

3. RESULTS

Throughout the formation of the statistical sample and data collection I made efforts to represent the opinion of all settlement categories and self- governments of different sizes within the study. In chapter 5.1, where I introduce the examined sample, I concluded that the elements of the sample will not be grouped by the type of the settlement or the number of its population regarding the size of the local government, instead, I have selected the average number of the staff to be the basis of the qualification, since it represents the size of the organization the best. As a result, self- governments are analysed by the categories of “micro”, “small”, “medium”

and “large”.

3.1. Characteristics of long term – strategic – planning

First I wanted to understand the purposes local governments aspire to achieve with planning. The results of the analysis indicate that in most cases (37% in general) they are fulfilling their legal obligations with planning.

The second highest result – 29% in average – was achieved by the answer that they prepare various plans for their own goals and interests. Other external factors also represent a significant share, with 16% in case of supervisory authorities, and 15% in case of obligations towards the European Union. For the leaders of the studied self-governments, the preparation of plans is only a means to fulfil legal obligations, and they do not feel the need to prepare other plans – not regulated by the law-, which would otherwise support an efficient and successful operation and administration.

In the questionnaire I enquired about the most typical types of plans applied in business, which self-governments also prepare. The various plans applied in the business sector can all be adapted to this sector as well.

11

Naturally when applying them we must take into account the peculiarities of the administration of governments, financing and the accounting information system.

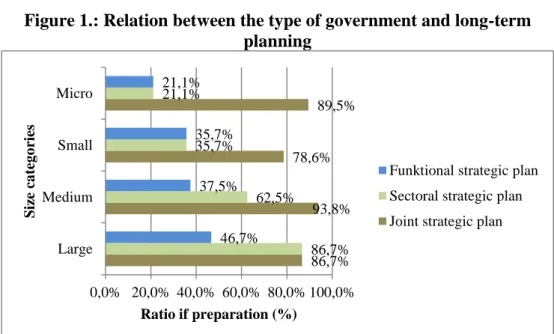

Respondents indeed implement long-term planning, 87,5% of them prepare joint strategic plans on the level of the government and its institutions, which I consider to be equal with an economic program. When observing the other levels of long-term plans, we receive less favourable results, 50%

of respondents prepare sectoral, and only 34,4 percent prepares functional strategic plans. When examining the answers based on the sizes (see figure 1.), the results are quite similar. The proportion of those who prepare joint strategies are between 79 and 94 percent in case of all size categories.

Sectoral strategic plans are most frequently constructed by large local governments (with 87%), and micro governments are the ones less likely to prepare it, with a proportion of 21 percent. The existence of functional strategies is also the lowest in this case – similarly to the aggregated results, their share is between 21 and 47 percent.

Figure 1.: Relation between the type of government and long-term planning

Source: own edition based on SPSS database

86,7%

93,8%

78,6%

89,5%

86,7%

62,5%

35,7%

21,1%

46,7%

37,5%

35,7%

21,1%

0,0% 20,0% 40,0% 60,0% 80,0% 100,0%

Large Medium Small Micro

Ratio if preparation (%)

Size categories

Funktional strategic plan Sectoral strategic plan Joint strategic plan

12

The next yes or no question was about whether local governments involved in the study perform formalized strategic planning.

The majority of respondents (57,81%) admits to implement formalized strategic planning, however the proportion of local governments to answer with “no” slightly exceeded the proportion of those who said “yes” in case of micro and small sized local governments (52,63% of micro self- governments, and 57,14% of small self-governments). 55,6% of self- governments who do not apply formalized strategic planning believe that its realization in the future would be reasonable. I believe that this ratio reflects a positive attitude regarding the future application of strategic planning.

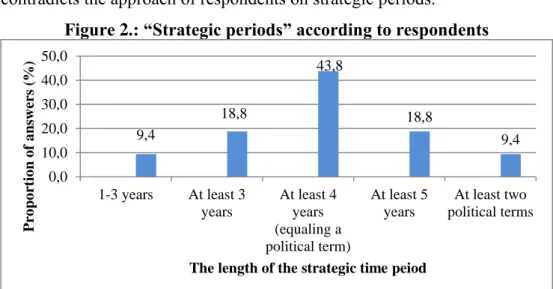

Nevertheless, the high proportion of the existence of formalized planning contradicts the approach of respondents on strategic periods.

Figure 2.: “Strategic periods” according to respondents

Source: own edition based on SPSS database

43,8% of respondents believe that a political term (4 years in Hungary) is considered to be a strategic time period, and only 9,4% of them agree that strategic planning must cover a period that lasts for the length of at least two political terms. Considering that political decisions have long-term effects in general, it is important that planning is not only about “tomorrow”, but it should bear in mind the wellbeing of future generations as well.

9,4

18,8

43,8

18,8

9,4 0,0

10,0 20,0 30,0 40,0 50,0

1-3 years At least 3 years

At least 4 years (equaling a political term)

At least 5 years

At least two political terms

Proportion of answers (%)

The length of the strategic time peiod

13

Further consequences of a short-term approach is that when the current leaders – elected representatives and officers – are characterized by short- term thinking and enforcement of interests, their chances to be re-elected decrease.

Now when the management of a town is replaced every 4 years, it is impossible to establish a future that is supported by strategic planning as well.

Naturally the examination of the existence of long-term planning cannot be based on solely these questions, since actual strategic planning is not limited exclusively to the preparation of strategic plan documents. Monitoring activities, continuous reporting, feedback and the revision of strategic plans and their necessary modifications all form an integral part of the planning process. Strategic plans supporting efficient operation in the long-term must be underpinned by the application of strategic analysis and planning methods which are already applied in the business sector and could be successfully adapted to local governments as well, otherwise strategic plans mean nothing but impractical concepts and promises which are impossible to keep for the members of the society, instead of well-designed plans which are mathematically founded as well, and could be realized successfully in the future.

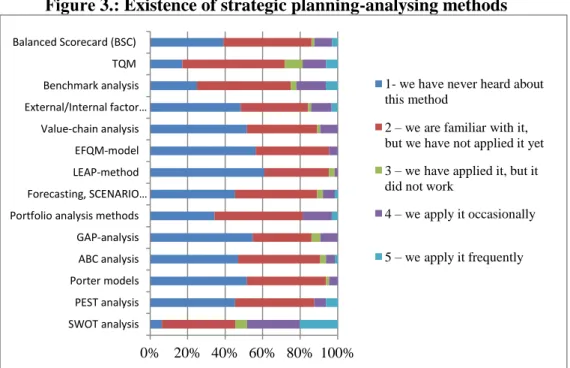

I attempted to assess the proliferation and frequency of the application of the most popular methods by governments, which can be applied during the elaboration of the strategy, with the help of a scale ranging from one to five.

The values of the scale were: 1 – we have never heard about this method; 2 – we are familiar with it, but we have not applied it yet; 3 – we have applied it, but it did not work; 4 – we apply it occasionally; 5 – we apply it frequently. The results are demonstrated by figure 3.

14

Figure 3.: Existence of strategic planning-analysing methods

Source: own edition based on SPSS database

The results of the questionnaire survey confirmed my preliminary hypothesis, that involved parties are completely unfamiliar with the strategic planning-analysing methods which are most frequently applied in the business sector (PEST analysis, Porter models, ABC analyses, GAP analysis, Scenario planning, LEAP, EFQM, value-chain analysis, external- internal factor evaluation matrix), or even if they have previously heard about a very few of the methods, they have never actually applied them in practice (such as BSC analyses, Portfolio method, TQM, Benchmark analysis). The most common method to be applied regularly was the

“SWOT” analysis with its 20,3% ratio. Based on the results of the question regarding the monitoring of the strategy, it turned out that the majority of analysed governments (57,8%) fails to implement strategic monitoring. It means that they do not track the completion of strategic goals through the measurement of indicators.

0% 20% 40% 60% 80% 100%

SWOT analysis PEST analysis Porter models ABC analysis GAP-analysis Portfolio analysis methods Forecasting, SCENARIO…

LEAP-method EFQM-model Value-chain analysis External/Internal factor…

Benchmark analysis TQM Balanced Scorecard (BSC)

1- we have never heard about this method

2 – we are familiar with it, but we have not applied it yet 3 – we have applied it, but it did not work

4 – we apply it occasionally

5 – we apply it frequently

15

This result also confirms the fact that the elaboration of a strategy is mostly motivated by conforming to an external force (such as a legal obligation) instead of strategic planning and management driven by their own motivations.

Conforming to this external obligation is primarily completed with the preparation of an economic program. After all, the results also indicate the lack of strategic management activities and their flaws.

The two basic criteria regarding planning are flexibility and realism, which both have to be present during the planning process. Plans must be reviewed continuously in order to see whether the set objectives are still realistic, and the designed actions and action programs are viable, or in other words, whether the plan is still feasible. In order to make if feasible, the foreseen impacts of environmental changes considered on a wider level must be adapted, thus plans must be updated continuously. In this sense, the review and maintenance of plans – including strategic plans as well – has to be a continuous and frequent activity, otherwise the basic criteria of flexibility and realism will not be realized in the process of planning. Experiences show that these two principles are not as much realized in the public sector.

Only 37,5% of respondents said that the revision of plans is a frequent, annual duty, while in case of 32,8% it is implemented in every 2-4 years.

Another significant share, 20,3% is represented by those who perform revision activities occasionally, on a non-regular basis. Nevertheless, 56,3%

of local governments participating in the study are satisfied with the realization of long-term goals and initiations.

Strategic planning in case of local governments – considering that the providing of services is both special and public – can only be efficient and serve the interest of the “public”, if the strategic objectives as the foundation of strategic plans are elaborated and approved by the cooperation of all stakeholders (involved parties).

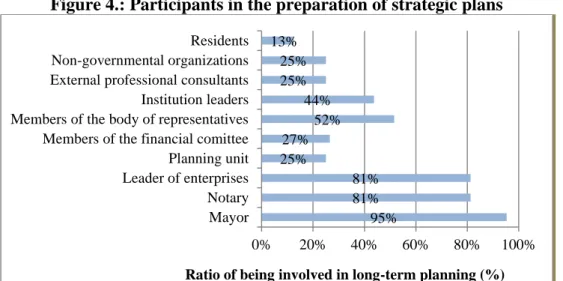

16

Based on the empirical data that supports this study, there is only a low level of such cooperation of involved parties in case of local governments in Hungary (figure 4.), since out of all parties, only the participation of the mayor, the notary and financial-administration leaders are determinant in the process of elaborating the strategy. It is recommended to ensure the active participation and motivation of other stakeholders in the process of long- term planning, thus establishing a planning process which is based on cooperation.

Figure 4.: Participants in the preparation of strategic plans

Source: own edition based on SPSS database

The strategic role of the economic program

The elements appearing within the economic program show a colourful picture, however the general conclusion is that the most frequent number – the modus of the sample – is “4”, which means that in most cases there are four different strategic elements identified in an economic program.

These four strategic elements applied the most frequently are:

Appointing strategic goals regarding the tasks, sectors which are of key importance for the settlement (81,3%).

95%

81%

81%

25%

27%

52%

44%

25%

25%

13%

0% 20% 40% 60% 80% 100%

Mayor Notary Leader of enterprises Planning unit Members of the financial comittee Members of the body of representatives Institution leaders External professional consultants Non-governmental organizations Residents

Ratio of being involved in long-term planning (%)

17

Assessment of the internal capabilities and skills of the government and its institutions (64,1%).

Vision, mission, philosophy of the self-government, strategic policies (60,9%).

Analysis of the external environment, strategic situation analysis, exploring the opportunities available for the government (59,4%).

The analysis of the self-government’s internal capabilities, characteristics and its external environment is basically equal to a SWOT-analysis. The result is in accordance with the results of the analysis on the application of strategic planning methods. With a two-sample T-test, I have analysed the relationship between how formalized planning is and the strategic foundations of the economic program. The results of the test show that the elaboration of a formalized strategy indicates a higher number of strategic elements present within the economic program. This hypothesis is valid on a confidence level of 5.7%, which is close to the accepted level of 5%. With further coherence analysis I attempted to find out whether a relationship exists between the size of the government and the frequency of the presence of the various strategic elements one by one. According to the results of the Chi-square test, this relationship with the size of the government only exists in case of action plans and the implementation of these actions, on a 7.5%

significance level, and with a 6.91 value of the test statistics. A statistical relationship also exists with the application of formalized strategic planning in case of this very same strategic element, on a 4.7% significance level, and with a 3.945 value of the test statistics.

As a conclusion, self-governments performing formalized strategic planning prepare action plans and actions within the frame of the economic program to a larger extent than those who do not create a formalized strategy, however this statement is not valid in case of the other elements of the strategy.

18

The objectives and programs defined in the economic program can only be considered realistic, when they are supported by actual calculations, and were elaborated in accordance with other elements of strategic management.

70.3% prepare financial plans, and 53.1% apply the instrument of executive summaries. At the same time, there is a same ratio (48.4%) for the preparation of return analysis and institution diagnosis, for the purpose of supporting the economic program. The majority of the documents mentioned in the question – resource allocation plans, functional and sectoral strategic plans, communication plans, strategic plans, expert estimations – are applied in practice on a very low level, the background of which should also be investigated. Therefore, as a conclusion I can say that the economic program of local governments includes very few actual strategic elements, independent from the extent of the application of formalized strategic planning. This result again confirms the hypothesis that self-governments do not implement actual strategic planning activities, and that the economic program cannot fulfil the role of a solid strategic plan.

Programs are prepared in accordance with the – minimal – mandatory content prescribed by the law about self-governments in force, however 66.7% of respondents agree that the relevant legislation should be more specific in details about regulations affecting the content and form of the economic program.

3.2. Short term – annual – planning

When analysing the short term – annual or shorter – planning practices, I came to a conclusion that due to the regulations on the planning of governments, the preparation of the annual budget is most frequently applied as the primarily financial plan. The preparation of a liquidity plan is also typical, with a cumulated average of 77 percent, the high proportion of which can also be explained by the effective regulations prescribed by the

19

law3. The preparation of plans regarding cash flow, purchase, maintenance, risk management, resource or other short-term plans represent an unsubstantial percentage, since none of the aggregated average proportions regarding short term plans exceed 40 percent. The lowest ratio, with an average of 25% is found in case of the preparation of cash flow. These comprehensive statements are valid when examining governments separately by their size as well. It is also important to see that 53% of large governments prepare plans and risk assessment, which might be explained by the large scale investments they have realized, and risk assessment and return calculations that are brought forward by the financing of EU investments and renovations.

As a summary, the emphasis of short-term planning is on the preparation of the annual budget and the planning of liquidity.

Throughout the analysis we aspired to see the exact number of the different type of plans that are applied in practice. According to the results, the analysed self-governments prepare “5 types of plans” in most of the cases (23%), followed by “4 types of plans” (in 17%) as the second most frequent practice.

When considering the number of mandatory plans, these results also demonstrate that local governments apply planning primarily with the objective to conform to legal obligations, and it is less triggered by their own motivations or management approach. All of this confirm my previous statements. The implementation of planning activities driven only by external forces contradicts the presence of strategy-driven management.

Regarding the planning of the annual budget as the most frequently prepared annual plan, the analyses has covered the examination of the methodologies as well.

3 Besides the preparation of the annual budget plan, the Áhtv. includes a brief note on the obligation of preparing a liquidity plan. (see Áhtv. 78.§ (2))

20

Amongst other issues, I have analysed the proportion of the practical application of planning techniques used in the preparation of the budget of local governments being included in the sample, and thus the level of its spread in practice. Respondents have been asked to distribute 100%

amongst the major methods of budget planning, based on the frequency of their application in practice. The results of the analysis are illustrated by figure 5.

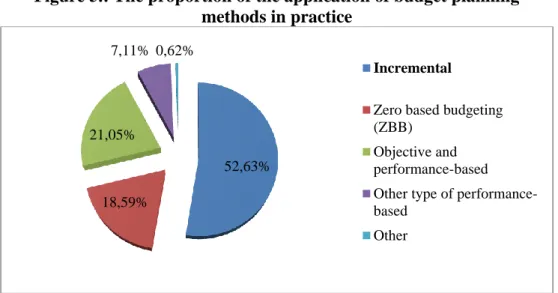

Figure 5.: The proportion of the application of budget planning methods in practice

Source: own edition based on SPSS database

Based on the literature about budget planning and its renewal (Báger, 2006;

Báger szerk.,2010; Csapodi, 2009; Tassonyi, 2002; Szalai, 2007), the most urgent and obvious fields of the improvement of planning systems are the renewal of the technology of the annual budget planning and the decrease of the dominance of incremental budget planning techniques and its differentiated application by the type of tasks. The statements of my theoretical research was confirmed by the empirical results of the study, since 51,6% of involved parties believe that budgetary planning is characterized by a basic approach, which has to be changed in the future.

52,63%

18,59%

21,05%

7,11% 0,62%

Incremental

Zero based budgeting (ZBB)

Objective and performance-based Other type of performance- based

Other

21

As it is demonstrated by figure 5., when considering the estimations about expenditures on mandatory tasks, the majority of local governments included in the sample, 52,63% of them apply incremental budget planning techniques, and the second most frequently used methods are objective and performance based (program) techniques with a ratio of 21,05%. The ZBB procedure is applied in case of an average of 18,59% of the local governments included in the sample. Within this group of questions, respondent governments applying objective and performance based planning methods were asked to appoint the tasks affected by program planning. By summarizing the answers, the most frequent tasks were the followings:

settlement development,

occasional projects, EU tenders

investment and renewal expenditures

residential old people’s home care

maintenance

mandatory public work planning

sports

basic health care services

social expenditures.

Out of the listed tasks, program based budget planning methods and approaches are used most often in case of settlement development and investment and development related tasks.

When asked “if you do not apply program based budget planning techniques, do you plan to use it in the future?”, the vast majority of respondents, 73,7% said no.

The results also testify my hypothesis that various budget planning techniques have to be differentiated to fit the task to be performed.

22

Based on this hypothesis, I also aspired to see how involved parties would differentiate budget planning methods amongst all mandatory tasks of local governments specified by the law in force.

By summarizing the results, there is an obvious – yet contradictory, compared to previous answers – picture, according to which, respondents believe the traditional basic approach planning technology to be the most efficient one to be applied with the majority of the government’s tasks, and they only consider the planning of budget expenditures within the frame of a program structure to be better in case of settlement development, cultural services and sports, youth and nationality related issues. The zero-based planning method was not selected as a frequently applicable method by any of the participants.

It is interesting that regarding the field of kindergarten and social care services and child protection, the ZBB method is preferred by respondents instead of program budgeting. These results reflect on a contradiction compared to results of the previous analysis, since they show that except for a few examples, those who are involved in planning are completely satisfied with having an incremental planning and they believe it to be the best method for allocating the budget amongst tasks.

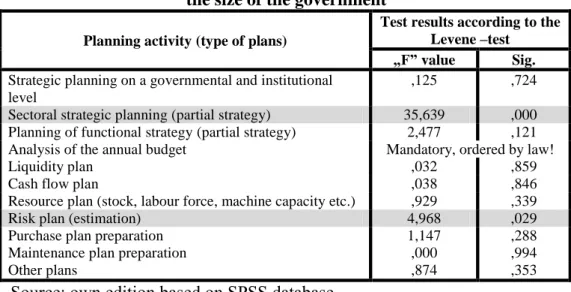

3.3. Role of the size of the government and the state of development of planning processes and methods

According to my hypothesis, there is no link between the size of the government and the “state of development” and characteristics of the applied planning practice, therefore performing a segmentation based on size is unnecessary here. First I wanted to examine whether the size of the self-government influence the application of the various types and levels of plans.

23

Table 1.: Results of the two-sample T-test between the type of plans and the size of the government

Planning activity (type of plans)

Test results according to the Levene –test

„F” value Sig.

Strategic planning on a governmental and institutional level

,125 ,724

Sectoral strategic planning (partial strategy) 35,639 ,000 Planning of functional strategy (partial strategy) 2,477 ,121 Analysis of the annual budget Mandatory, ordered by law!

Liquidity plan ,032 ,859

Cash flow plan ,038 ,846

Resource plan (stock, labour force, machine capacity etc.) ,929 ,339

Risk plan (estimation) 4,968 ,029

Purchase plan preparation 1,147 ,288

Maintenance plan preparation ,000 ,994

Other plans ,874 ,353

Source: own edition based on SPSS database

The results indicate that when seeking for a relationship by the type of plans, a link between the size is only detected on a 5% significance level in case of the preparation of sectoral strategic plans and risk plans including risk assessment, and the null hypothesis about the identity of the deviation is not valid regarding the other plans. In relation to the size I have performed a separate analysis on the relation with long and short term planning, grouped by:

links between the size and the attributes of long term planning,

and links between the size and the attributes of short term planning.

Table 2.: Planning attributes involved in the analysis by the “size”

Attributes of strategic planning Attributes of annual (operative) planning

strategic approach of the management presence of formalized strategic planning

application of strategic planning methods presence of budget planning methods strategic monitoring

Source: own edition based on SPSS database

24

The strategic approach of the management is described by the strategic features of the management, with a detailed analysis introduced in chapter 5.2.1.1. Statistical analysis has been conducted with a variance analysis, and my previous hypothesis was confirmed by the result, meaning that there is no significant difference between the approach of the management of larger governments with a more complex organization, than the management approach of leaders of small organizations. The strategic approach of leaders does not depend on the size of the organization, but presumably on the personality, attitude, professional expertise of the leader, which all influence the presence of strategic thinking.

The assumed results have been confirmed by the statistical independence analysis performed in connection with the other factors. With the help of the independence analysis performed with the SPSS program, I was seeking for the relation between the size of the local government and the application of formalized strategic planning and the tracking of strategic plans. The statistical analyses demonstrated a low level of relation when performed on a significance level of 22,1% with a 4,4 value of the test statistics, meaning that there is no statistical relationship between the size of the government and the application of formalized strategic planning in practice. There was also no relationship found between the tracking (monitoring) of the completion of strategic objectives within the entire length of the strategic period and the size of the government. The results demonstrate that this relationship exists on a significance level of 28,5% with a 3,792 value of the test statistics. I believe that the appearance of continuous monitoring implemented through the indicators of the plan objectives is linked to the application of formalized strategic planning, and is not dependent on the size. With a cluster analysis I have performed further examinations in order to find out whether there are actual clusters based on the experiences of the application of planning methods and the size.

25

The final clusters have been formed with the help of a K-means algorithm within the frame of a non-hierarchic method.

In the process of clustering, the program ended the merging process at the 61. step, resulting in 3 clusters. The clustering process grouped the governments of different sizes based on the frequency of the application of strategic planning methods. The majority of the sample elements (about 80%) have been grouped in cluster number 3, irrespective to their size. The results show that the values of cluster number 3 are below the average values and those of the other two clusters regarding both planning methods, which means that the majority of governments as a group in general show unfavourable results in terms of the application of the methods.

Finally, I have also examined the differences between the application of short term planning techniques, in terms of the size. Chapter 5.2.1.4.

explains the results, according to which, an incremental budget planning approach prevails throughout the preparation of the annual budget. I tested my initial hypothesis with variance analysis, separately for each mandatory government task specified by the relevant legislation. The results indicate that the null hypothesis is rejected in case of most of the tasks, therefore there is no significant relationship between the size of the government and the applied budget planning method. A significant relationship was detected in case of certain tasks, such as the operation of the settlement, defence, civil protection, disaster management and ensuring the public safety of settlements. With the implemented F-test I have received those tasks where there is a significant difference between the size of the government and the planning method. I have quantified the deviations between the group averages with the Bonferroni test, in order to see the actual differences between the budget planning techniques.

26

3.4. Factors of receptivity towards innovation

In the final part of the questionnaire I attempted to understand the opinion of governments on the further development of their planning systems. More than half of the governments (59.38%) show openness and feel that it is necessary to improve their planning systems in the future. The inclination towards innovation is represented by the openness towards the improvement of the planning system, in my opinion. I have investigated the validity of factors influencing the inclination towards innovation, based on the results of an international research (Berry, 1994). These assumed factors are the financial situation, openness, regional position and management approach.

Table 3.: Factors of inclination towards innovation

Factors

Value of Chi- square

Degrees of freedom

Significance level

Proportion of expense gross sum 5,196 4 ,268

Debt ratio 5,087 2 ,079

Relation with the private sector 3,627 2 ,163 Relation with the sector of self-

governments 1,182 1 ,277

Influence of the innovation

practices of other governments ,273 1 ,602

Source: own edition based on SPSS database

The previously assumed correlations have not been confirmed by the Chi-square test, which – in terms of statistics – means that I have to accept the null hypotheses and also reject the existence of stochastic relationships between the assumed qualitative attributes.

As the final step in the examination of factors influencing the inclination towards innovation, I have analysed the existence of a statistical relationship between the management approach of the leadership of the government, and the strength level of strategic thinking and the openness towards innovation.

In my research I assumed that leaders with a strategic approach are more innovative and open, since receptivity towards innovation requires a manager approach with strategic goals.

27

In order to express the management approach, I have analysed the answers received for question 2.3 of the questionnaire (for detailed analysis see chapter 5.2.1.1.). For this analysis I have performed a two-sample T-test, and my previous hypotheses have not been statistically confirmed on a confidence level of 5%.

3.5. The future of planning

In order to provide a comprehensive evaluation of the planning system, I have composed 8 statements, which had to be evaluated on a nominal scale from 1 to 3. The options for grading were 1 – not true, 2 – true, but does not require modification and 3 – true and requires modification. By summarizing the results of the submitted answers it is obvious that there are only two scenarios when respondent governments feel that a change would be necessary. In case of the 1. statement (The incremental approach is dominant during the planning of the budget), and the 7. one (The planning system fails to ensure transparent administration and the balance between the public duties to be performed (expenditures) and resources of financing (revenues)), where option “number 3” was dominant, with a ratio of 51,6%

and 43,8%. Regarding the remaining six statements, respondents admitted that the statement is true, yet they felt it does not require any modification or improvement in the future.

I believe that stakeholders are afraid of innovation, because as the first step of development it is recommended to perform an efficiency screening on the planning process, which might imply the risk of reduction within certain elements and scope of duties of the process (lean approach), which might also result in the reorganization or even the in the termination of the scope of duty in question.

With the last round of questions in the survey we attempted to examine the intention of further developing the planning system, the potential fields regarding the innovation of the planning system and also those

28

recommended by governments, within the frame of multiple choice questions.

The introductory question investigated whether respondents “plan to improve the planning system in the near future”. We have received favourable answers, as the development of the planning system is included in the short term objectives in the majority of the cases, which is 59,4% of respondents. The majority of respondents marked “three” – in 20,3% - or

“four” – in 18,8% - fields for development. Key fields for the innovation of the planning system from the perspective of stakeholders are the establishment and improvement of the strategic planning process – in 65,8% - and the development of the budgetary technique, shifting it towards an objective and performance based planning – in 71,1%. The majority has not preferred the remaining fields of development, or do not feel that these fields require improvement.

In relation to the issue of improvement, I have drafted questions about controlling as well. The results of the empirical research show that 84.4% of respondents agree with the statement that a controlling system is able to efficiently support the complex planning system of a self-government, and 73.4% of them also believe that controlling can support the successful implementation of strategic and operative plans, and an operation which is able to create values, irrespective to the size of the government.

Despite the positive attitude shown towards controlling, only 18.8% of the self-governments involved in the examination operate controlling systems and apply controlling methods. This proportion is very low.

82.7% of respondents answered the question “why don’t you use a controlling system” with the option “I am familiar with controlling and I feel that its introduction is necessary, but it has not been implemented yet due to the lack of time and resources”, and there is only a 15.4% of respondents who is familiar with controlling, but does not feel its

29

introduction to be important, since they are satisfied with their current activities regarding planning, analysis, monitoring and information management.

In case of those few self-governments who introduced controlling, it was justified with the following reasons:

It supports the economic, efficient and successful operation and administration of the government (the completion of requirements of the so-called “3E” approach).

Improves the transparency and accountability of administration.

Efficiently supports the future-oriented, resource- and cost-oriented, strategic management activities of the self-government and of the leaders of its institutions.

In order to confirm the results of the quantitative research, I have also conducted structured deep interviews. I had two major aspects when selecting my interviewees, one was professionalism, and the other is the differentiation by size. The subjects of my interviews were – typically – leading associates who are involved in the planning process. I also took care of selecting interviewees from all government size categories, as I wanted to know the personal opinion of associates representing the various sizes of governments, thus I have been able to examine my previous hypotheses regarding the differentiation by size. The questions asked throughout the deep interview are listed in annex number 2. of the study.

As a conclusion, the results received from the deep interviews confirm my preliminary hypothesis, and are in accordance with the results of the quantitative research.

30

4. CONSEQUENCES

Available literature and researches in the topic of planning system within the sector of governments mostly focus on the methodology of the preparation of the annual budget (planning), theoretical questions and practical examination (for example: ÁSZ studies), and pay less attention to strategic planning issues implemented on the level of local governments.

This dominance of the budget was confirmed by the results of the empirical study as well. The short term approach applied in the planning process is also reflected by the fact that the long term goals, ideas for development, the conditions for operation and the performance of tasks are not appointed along strategic goals, but based on the funding opportunities available at the time of planning. The plans prepared during the planning process serve as the basis for administration and operation, and this statement is especially true in case of self-governments. The current planning system is outdated, and it fails to fulfil its basic role, the ensuring of a transparent administration and balance between the public services to be performed (expenditures) and resources of financing (revenues). I believe that one of the greatest risks, dangers in the planning system of self-governments is short term thinking, and the excess dominance of the planning of the annual budget, since in the absence of a strategic approach and strategic planning, this activity will only focus on the present, or the past, therefore the present determines the completion of duties, and the constant operation.

In the business sector, the unpredictable changes in the environment and the strong market competition causes the traditional – time consuming, costly and static corporate planning to be outdated. In today’s economy, the most important advice for enterprises is that they must recognize the expected changes in due course, and that they have to be able to manoeuvre without delay when necessary.

31

It requires the planning activity to be swift and efficient, and to enable flexible reactions. What characteristics should modern planning systems bear in case of local governments?

I believe that the modern planning process is not characterized by a forced

“short-term approach”. Planning is rather a process, which is available for local leaders as a management instrument, an opportunity ensuring long term development and survival. Therefore the first step of the development must be the reinterpretation of planning, with more focus on the management approach. Recommended orientations for modern planning systems: future-oriented, complex, well-founded, cooperative, flexible, objective, productive and transparent. The planning system must be defined by a sustainable strategic planning process, which also supports valuable public services in the long term, based on the economic program. Another criteria is that the planning process and plans have to be well founded. In terms of methodology, an appropriate planning process should combine the various planning-analysing methods optimally, and should cover all dimensions of time, with well-designed indicators assisting the monitoring of the implementation of plans, also providing constant feedback for leaders.

The operation of a government can best be described by the objective of an efficient, successful and economic operation – applying a “3E” approach.

The completion of this objective could best be ensured by the operation and administration of the self-government based on a developed planning system. A modern planning system could be established and operated successfully within the frame of a controlling system, based on the budgetary accounting information system complemented with the management accounting sub-system. In my dissertation I have drafted the structure and orientation of a modern planning system.

32

5. NEW AND RECENT RESEARCH FINDINGS

Based on the performed empirical research and the procession of relevant legislation and national and international literature, the following new scientific statements can be made:

1. Long term plans are prepared by local governments – typically in order to complete their legal obligations -, yet there is no actual formalized and complex strategic planning process implemented.

The methodology behind long term plans is not well-founded, the tracking and monitoring activity of the realization of objectives defined in strategic plans is implemented on a low level, and the participation of a wide range of involved stakeholders is not realized within the process of creating a strategy.

In order to confirm my statement, I have analysed the answers received from the questioners distributed to self-governments, and the experiences of the deep interviews, with the help of descriptive statistic methods and coherence analysis.

2. The results obviously indicate that currently the economic program cannot be considered as an actual strategic management instrument to support a future-oriented management decision making process.

Throughout the preparation of the program, strategic planning and management techniques are not applied, therefore plans cannot be considered as well-founded and well-prepared. At the same time, the economic program is able to fulfil the role of a joint strategic plan of a self-government and its institutions, which must be completed with other functional plans (by the functions of government) and resource strategic plans, therefore a consistent system of strategic plan documents can be established.

33

I recommend – in accordance with the majority of respondents – that the relevant legislation should be more specific in details about regulations affecting the content and form of the economic program, and I also recommend that the time span covered by a program should mandatory cover two political terms. I also make proposals for the structure of the economic program in my study. My statements are confirmed by the studying of relevant legislation in force, the content analysis of the deep interviews conducted with stakeholders, and the statistical analysis of the replies submitted for the questionnaire survey.

3. The application of program planning is on a low level in the current budget planning practice. With the help of program planning, budgetary funds granted for the financing of tasks are more substantial in terms of economics, and the completion of the objectives defined in strategic plans can also be monitored. Programs built from specialised tasks should be established according to the qualification of “COFOG” (government functions), in accordance with the orders of the new accounting regulation.

In my dissertation I have made proposals for the structure of program-based planning systems, and also regarding the differentiated application of budget planning methods.

34

4. Regarding the comprehensive analysis and the further development of the planning system of local governments there is no need for performing a segmentation based on size. The development state of the planning system of local governments show a completely uniform picture regarding the applied planning methods, plan documents, and the level of formalization. The application of modern planning-analysing methods based on strategic planning – strategy orientation – is necessary, irrespective to the size of the government.

This relationship analysis has been carried out with a Chi-square test, cluster analysis and variance analysis. After performing the statistic independence analysis I have received the assumed results.

5. The intention for the further development of the planning system (inclination towards innovation) – despite my previous assumption – did not show any causal link with the financial situation, openness and regional position (altogether: environmental effects) and with the factors of a management approach.

Based on my preliminary hypothesis – which I have drafted along the findings of international researches – the combined impacts of the financial situation of local governments, the level of cooperation shown towards the private sector (openness), the impacts (regional spread) of innovations introduced at neighbouring governments (best practices), and the existence of a management approach influence the intention of governments for innovation. However, these assumptions have not been confirmed by the implemented statistical analysis, correlation tests and deep interviews.

Nevertheless, the final results of the analysis further strengthen my statements made in relation to the size of the government (new result number 4).

35

6. PROPOSALS (THEORETICAL AND PRACTICAL APPLICATION

In my study I attempted to introduce the foundations of an alternative planning approach, which is on one hand built on the practical elements of management methods, and at the same time it considers the traditions of budget planning as well.

I have the following comprehensive innovative proposals for the further development of the planning system:

Prior to the first step of development we must answer the basic question

“what do we expect from planning”. The right answer might be that the benefit measurable throughout the implementation of plans should be in accordance with the expectations of “stakeholders”. Benefit in this sense equals the impact (outcome) on stakeholders – also being set amongst the preliminary objectives.

The strategic approach and strategic management activities must be strengthened, along with the transformation of strategic planning and analysing methods to be adaptable for local governments. Within the frame of this, the first step should be the strengthening of the global strategic role of the economic program, covering the whole operation of the government. A Balanced Scorecard (BSC) prepared for each program is the best method to support the completion of objectives set in strategic plans, and thus strategic management activities. Besides the application of BSC, we recommend the continuous implementation of other methods such as the SWOT, and Benchmarking methods. With the help of these methods, it is possible to operate a complex strategic planning-analytic-decision supporting system within the frame of strategic controlling.

36

The renewal of the budget planning technique, its differentiated application for each task and shifting towards performance and result oriented budget planning. I introduce the basic principles and process of program planning in my study.

Task financing requires planning on a task level, the management of tasks by the cost bearer and the performance of a cost-benefit analysis – or if possible, of revenue report – by tasks. Differentiation should be implemented depending on the various phases of the operation and the completion of duties, and the nature of the expenditure. The nature of the duty to be performed and the structure of expenditures have a fundamental influence on the planning technique to be applied.

Linking strategic plans with the annual budget, the establishment of a measurable causal relation system. The imprints of the strategy are reflected by the preferences of the expense side in annual budgets. The measurability and traceability of the realization and completion of the causal relation and strategic objectives (figures) in the annual budget is supported by the complex strategic – tactical and budgetary planning system established within a program structure, and it is recommended to be established within the frame of BSC.

The establishment of a cooperative planning system with the involvement of a wider range of stakeholders (e.g.: local enterprises, other administration organizations, non-governmental organizations, residents). Public hearings organized by local governments might provide an excellent opportunity for this, which must be well promoted in advance, in order to be able to deliver all the necessary information to stakeholders in due course.

Owing to the recent changes in the legislation of accounting, the information basis for a management accounting has been created in the public sector as well.

37

Management accounting to be established within the budgetary sector is interpreted in my opinion as a system which supports the provision of information and the creation of values, with the objective of providing information required for the completion of duties for the various levels of the management, in order to ensure economic, efficient and quality public services. In my dissertation I have made proposals for the establishment of a management accounting sub-system. I believe that the connected processes of planning, analysis and information supply should be organized with the conscious application of the methods of a management accounting sub-system, and within the frame of controlling.

After studying the relevant legislation and the results of the empirical research, I have drafted my proposals on the modification of the legislation as well.

1. The liberty and freedom of local governments enabled by the current legislation regarding the form and content of the economic program is way too large. I believe that it would be of great use to attach a well- structured document as an annex to the legislation, with the title

“content elements of the economic program”, and this fixed structure then should be filled out by governments, taking into account their individual peculiarities. The majority of respondents agreed with my proposal. The unified structure of economic programs would enable governments to perform comparing analyses, and it would also be of great assistance for those who have to prepare it. The period covered by the program should last at least two political terms, considering the strategic nature of the program. Regarding the specifications for its form and content, I consider the government regulation number 314/2012 (XI.8.) – on urban development concept, integrated settlement development strategy, instruments of urban planning, and the special