and international investment position statistics

2014

and international investment position statistics

(revised international methodology and national practice)

2014

Published by the Magyar Nemzeti Bank Publisher in charge: Eszter Hergár H-1054 Budapest, Szabadság tér 9.

www.mnb.hu

ISBN 978-963-9383-98-2 (online) 2014

Prepared by the Statistics Directorate of the Magyar Nemzeti Bank The manuscript was closed in September 2014

Published by the Magyar Nemzeti Bank Publisher in charge: Eszter Hergár H-1054 Budapest, Szabadság tér 9.

www.mnb.hu

ISBN 978-963-9383-98-2 (online)

Introduction

5List of abbreviations

61 Overview of international methodology

71.1 Key concepts and accounting framework of the balance of payments and international investment position statistics 7

1.2 Structure of the balance of payments 9

1.2.1 Current account 10

1.2.2 Capital account 14

1.2.3 Financial account 15

1.3 International investment position 18

1.4 Balance of payments in the macroeconomic statistics framework, links to the system of national accounts 19

1.5 Major changes from the previous edition 22

1.5.1 Necessity of the new edition 22

1.5.2 Harmony with the national accounts 24

1.5.3 Changes in the classification of financial instruments 25

1.5.4 Significant changes in classification within functional categories 25

1.5.5 The structure of the new balance of payments manual 26

2 National practice in Hungary

282.1 Methodology of the compilation of the balance of payments and international investment position statistics 28

2.1.1 General remarks 28

2.1.2 Major components and instruments in the balance of payments and international investment position 30

2.1.2.1 The current account 30

2.1.2.2 Capital account 37

2.1.2.3 The financial account and the international investment position 38

2.1.2.4 The statistical error 46

2.1.3 Methodology and special aspects of Hungarian practice 47

2.1.3.1 Treatment of Special Purpose Entities (SPEs) in the balance of payments statistics 47

2.1.3.2 Capital in transit and asset portfolio restructuring 49

2.1.3.3 Treatment of transactions relating to VAT registration 50

2.1.3.4 Methodology of the applied CIF/FOB adjustment 52

2.1.3.5 Methodology of the applied COPC adjustment 52

2.1.3.6 Accounting for EU transfers 54

2.2.3 Data processing system 60

2.3 Release and revision of balance of payments statistics 61

2.3.1 Release calendar 61

2.3.2 Data revision policy 63

3 Effect of implementing the new methodology on the balance of payments

and the related stock data

653.1 Effects of the BPM6 methodology on the financing capacity calculated from above 67

3.1.1 Goods and Services 67

3.1.2 Changes in primary and secondary income 68

3.1.3 Changes in the capital account 69

3.2 Effect of the change in methodology in the financial account and in the stock data 70 3.3 Retrospective data revisions performed simultaneously with the change in methodology 71

Annex 1

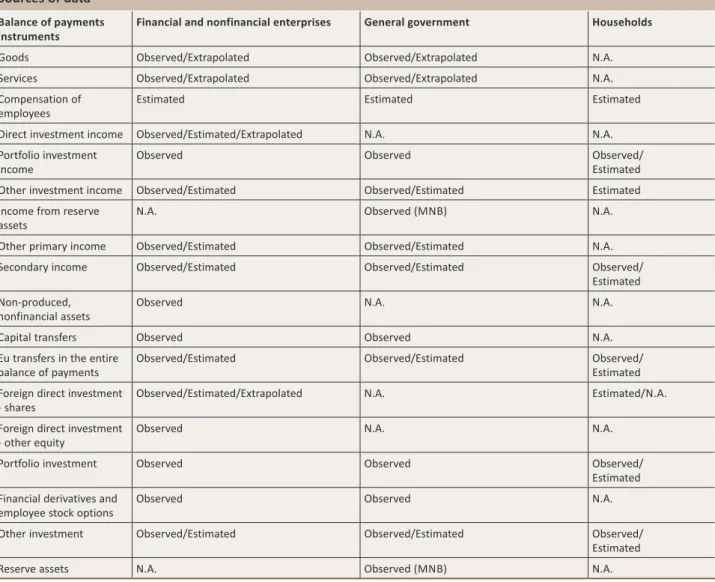

75Data collection for the compilation of the balance of payments statistics by subject area 75

Annex 2

78Notes on the classification of data of 1990–1994 in a new structure 78

Appendix

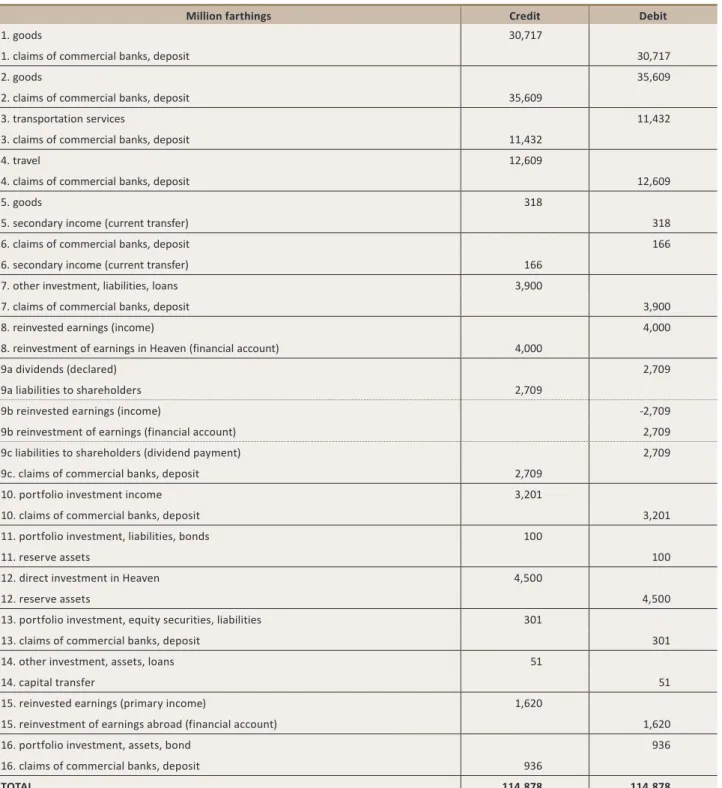

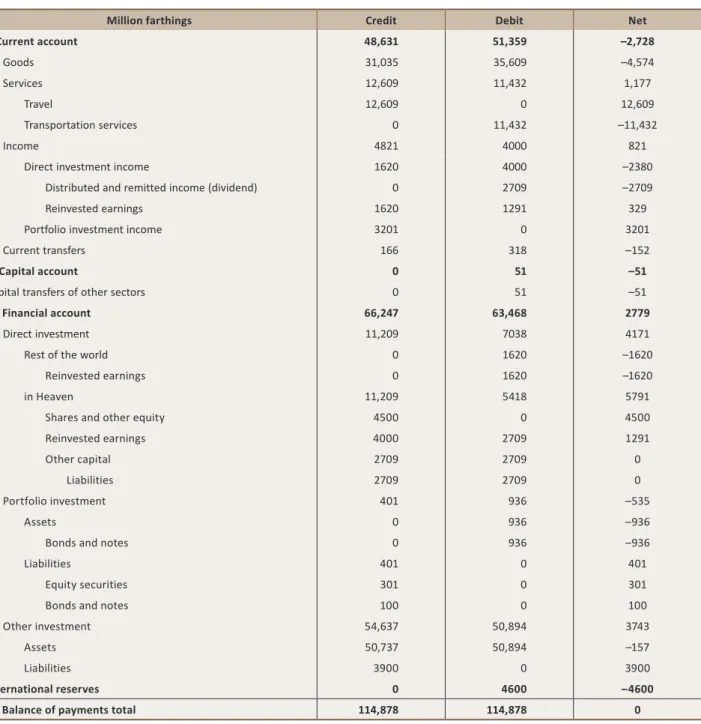

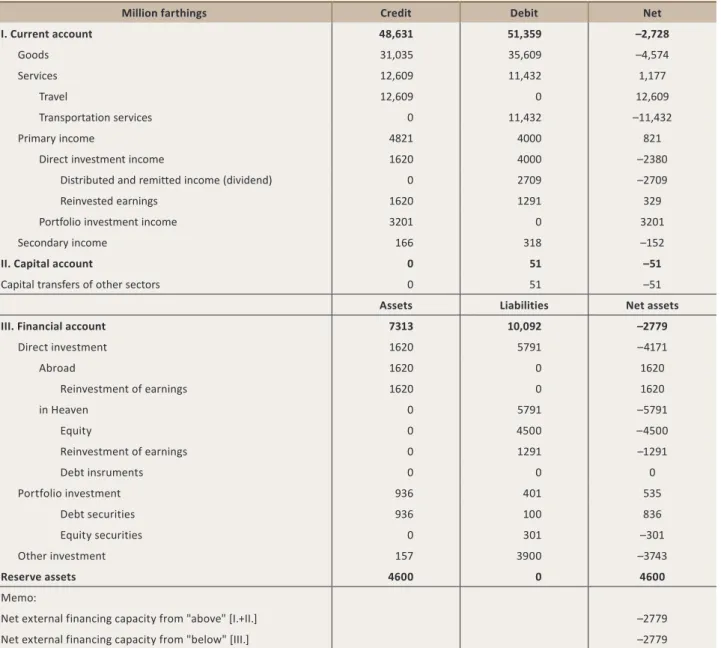

80Example for the compilation of the Balance of Payments and International Investment Position 80

Explanation of important special terms used in the publication 87

References 88

The Magyar Nemzeti Bank’s Statistics Directorate is now publishing Hungary’s Balance of Payments and International Investment Position Statistics (hereinafter the Publication) for the third time, to provide information to a wide range of users on the international methodology of the balance of payments and international investment position statistics and to explain the method of compilation of these statistics in Hungary. The reason for the updated release of the Publication within such a short period is that, in the European Union Member States, the changeover to the new statistical methodology which better reflects the current developments of the world economy (such as the spread of globalisation, the increased role of multinational corporations, free flow of capital, etc.) took place in 2014. The joint BPM6 changeover date within the EU was also coordinated with the implementation date of the new European System of Accounts (ESA 2010), which was revised in line with the new System of National Accounts (SNA 2008).

This Publication presents and explains the key concepts and conventions relating to the balance of payments and international investment position statistics as well as the structure of statistical reports and the conventions applied in their compilation.

The explanation of the relationship with the system of national accounts is of fundamental importance for understanding the system of macroeconomic statistics and in particular understanding the role of balance of payments statistics. Implementation of the new methodology has changed the structure of the balance of payments statistics in such a manner that the applied conceptual framework has been brought even closer to the system of national accounts. This is also manifest in renaming the major subaccounts (usage of primary income and secondary income in the balance of payments, as opposed to the former terms of income and current transfers), and the integration of the balancing items (net lending/net borrowing) into the standard structure. Chapter 1 focuses on the presentation of the international methodology.

In addition to presenting the international methodology, the MNB also wishes this Publication to present the national practice applied in the compilation of external accounts statistics. As part of that, in Chapter 2 we deal with Hungary’s specialities in terms of the system of data collection, processing and release.

The MNB website always discloses the most recent balance of payments and international investment position figures; therefore there is no annex to this Publication devoted specifically to statistical figures. However, the effect of the BPM6 changeover on the major aggregates is presented in Chapter 3.

Similarly to the previous edition in 2012, there is a special annex containing the complete list of monthly, quarterly and yearly reports to feed into the compilation of the balance of payments statistics. According to the accounting under the new methodology, we also updated the Appendix, where interested users can follow specific examples for monitoring the technical steps related to the statistical treatment of individual transactions. At the end of the Publication there is a section with brief explanations of the key special terms and a list of useful references to outside sources.

The various chapters of the publication were written by staff members of Magyar Nemzeti Bank Statistical Directorate working on balance of payments and international investment position statistics, namely: Péter Bánhegyi, Mihály Durucskó, Magdolna Kanyóné Pető, Beáta Montvai, Vanda Simonné Tánczos and Erika Veitzné Kenyeres, while the data available on the MNB website were compiled by János Basa, Gyöngyi Lipcsei and Dóra Bräutigam. The Publication was authorised by Director Ágnes Tardos.

Acronym English meaning

BD Benchmark Definition of Foreign Direct Investment

BOP Balance of Payments

BOPCOM Committee on Balance of Payments Statistics BPM5 Balance of Payments Manual Fifth Edition

BPM6 Balance of Payments and International Investment Position Manual Sixth Edition c.i.f. cost, insurance and freight

COPC Current operating performance concept

EGR EuroGroups Register

ESA European System of Accounts Extrastat Extrastat

f.o.b. free on board

FDI Foreign direct investment

FDIR Framework of Direct Investment Relationships FISIM Financial intermediation services indirectly measured IIP International Investment Position

Intrastat Intrastat

NEO Net errors and omissions

SDDS Special Data Dissemination Standard SNA System of National Accounts SPE/SCV Special Purpose Entity TÁSA Corporate Tax Declaration

methodology

1.1 KEy CONCEpts ANd ACCOuNtINg frAmEwOrK Of tHE bALANCE Of pAymENts ANd INtErNAtIONAL INvEstmENt pOsItION stAtIstICs

The balance of payments (BOP) is a flow-oriented statistical statement for recording economic and financial transactions between resident and non-resident institutional units of a country in a given period of time. Closely related to the flow-oriented balance of payments is the stock-oriented international investment position (IIP), which is a summary of statistical information on the stock of financial assets and liabilities vis-à-vis non-residents. The value of stocks may change between two reference dates due to transactions, revaluations resulting from changes in exchange rates and in the market prices of instruments or as a result of other changes in stock. The net worth of a country consists of the entirety of nonfinancial assets on the one hand and the net external financial position on the other hand, the latter being the difference between financial claims (+ gold bullion held as reserve assets) on and liabilities to the rest of the world. The net external financial position is presented in the international investment position. Balance of payments and international investment position statistics provide for the coherent recording of the transactions and financial positions of an economy vis-à-vis the rest of the world, portraying real economic and financial transactions from the perspective of the compiling country.

The concept of residence, in conformity with other macroeconomic statistics, is defined in the balance of payments statistics using the concepts of centre of predominant economic interest and economic territory. A resident of a given country is any natural or legal person or unincorporated entity whose centre of predominant economic interest (permanent residence, registered office, permanent establishment, production, etc.) is related to the economic territory of that country. Therefore, in statistical terms, the resident status of an economic unit in a given country depends on the existence of the centre of predominant economic interest rather than citizenship or nationality. From the perspective of an enterprise, this includes having a registered permanent establishment in the given country and engaging in economic activities there or, for new companies, intending to do so for at least one year.

Similarly to business accounting, the accounting framework of the balance of payments statistics is based on a series of conventions. One of the most important conventions is the principle of double-entry bookkeeping. Each recorded transaction is represented by two entries: the business event itself and the related financing, as a debit or credit entry, are recorded in the statistics (See Figure 1). In the overwhelming majority of transactions recorded in the balance of payments, nonfinancial or financial assets of a certain value change ownership in exchange for nonfinancial or financial assets of identical value. In case of financial assets, in addition to the change of ownership, the incurring of new claims and liabilities (e.g. bond issue) or their termination (e.g. debt repayment) or renewal with new conditions (e.g. amendment of maturity) by the contracting parties are also parts of the balance of payments. There are transactions when the counterparty gives nothing in exchange for the economic value supplied (e.g. food, medicine or investment aid). As the principle of double-entry bookkeeping is universally applied, the transactions related to these events must also be recorded in a two-sided arrangement. If no offsetting item is provided for a good, service or financial instrument, the missing ‘financing’ side of these unrequited transactions appears in the balance of payments as a transfer. If the unrequited transfer affects accumulation, it constitutes a capital transfer to be included in the capital account; otherwise it is a current transfer to be represented in the secondary income subaccount of the current account.

Following from the principle of double-entry bookkeeping, on an aggregated level, i.e. on the level of the balance of payments as a whole, the sum of all credit entries (total inflows) is identical to the sum of all debit entries (total outflows), i.e. balance of payments statistics, by definition, have a zero balance. Put another way, theoretically, the sum of the balances of the current account, the capital account and the financial account is always zero.

In the balance of payments statistics, in the aggregate presentation the current account and the capital account contain gross flows, while in the financial account balances are provided instead of the flows (credit/debit) for each financial instrument:

the net acquisition of financial assets and the net incurrence of financial liabilities. In the financial account of the published balance of payments statistics, this eliminates the consequence of the convention on signs (though it continues to apply on the transaction level) that signs indicate an increase or decrease depending on whether they are applied to assets or liabilities.

The increase of financial assets and liabilities are presented with the ‘+’ sign and their decrease with the ‘–’ sign. Consequently, the balance of the financial account is equal to the aggregate balance of the current and capital accounts, which itself is the balancing item of net lending (+)/net borrowing (–), calculated from below and above, respectively.

Compliance with the principle of having equal total debits and credits would only be possible if the balance of payments statistics were compiled on a transaction-by-transaction basis, in which case conformity with the principle of double-entry bookkeeping would be assured for each transaction. In practice, however, statistics are compiled from different data sources (reports from banks, companies, etc.). There can be differences between data sources in terms of valuation, timing and other aspects; furthermore, as a consequence of possible errors in recording, identity can only be accidental, thus reconciliation can only be subsequent and formal. This fact itself is independent of the features of the statistical information system, and it only expresses that real economic developments and their observation, unlike theory, are much too complex to facilitate the

figure 1

Convention of the double-entry system at the individual transaction level in balance of payments statistics

Credit (+) Debit (-)

export of goods and services inflow of income

received unrequited transfers decrease in assets

increase in liabilities

import of goods and services outflow of income

provided unrequited transfers increase in assets

decrease in liabilities

The changeover to BPM6 has not resulted in any changes in the treatment of individual transactions; the treatment in accordance with the principle of double-entry book-keeping continues to apply as before: for every ‘credit’ (CR) item there is a related ‘debit’ (DR) item, in other words, there is an inflow for every outflow, or – in the framework of the balance of payments statistics interpretation – a financing transaction belongs to every underlying transaction. (See the example in the Appendix for the technical details of the recording of individual transactions). What has changed compared to the earlier practice is the way the individual items of the financial account are reported. The sign of items in the financial account has changed, and according to the new methodology, in the financial account, the sign of the balance of assets and liabilities will show their impact on the stocks. Thus, the balance of the individual financial instruments shows a change in net assets as the difference between the balance on assets and liabilities (as opposed to the change in net liabilities applied so far). This is exactly the opposite compared to the net liability-type content of the BPM5 balance of the financial account. Therefore, the balance of the financial account in BPM6 shows net lending/net borrowing exactly the same way as the combined sum of the current account and the capital account. Accordingly, for example, the positive sign of the data of the financial account means an increase in net assets, which equals a net decrease in external liabilities and the outflow of resources.

box 1

the sign convention on the level of individual transactions and aggregate presentation

acquisition of perfect and comprehensive information on each and every event. This is the reason why each country’s balance of payments statistics include a line to reconcile the debit and credit sides, ex post and in formal terms, on the level of the balance of payments as a whole. This line is called ‘net errors and omissions’ (NEO). This balancing item may have either a positive or a negative sign depending on what is required to correct the statistical error. If the error is permanently in one direction or if its magnitude increases, this may be an indication of imperfections or errors in the data collection system.

When compiling international statistics, as the uniform assessment of transactions, the methodology considers the market price determined by the generally unrelated economic agents who participate in the transaction as the basis of recording.

A transaction must be recorded in statistics when the ownership of the nonfinancial or financial asset is transferred between residents and non-residents and when the relevant claim or liability is created, extinguished, transferred, etc.

The change of ownership, involving nonfinancial and financial assets, between residents and non-residents as the main criterion for recording the transactions in the balance of payments statistics indicates that the balance of payments, as opposed to what its name would suggest, constitutes statistics on an accrual basis, rather than on a cash basis. The recording of a transaction and its timing is determined by the date of change of ownership (or in the case of services the date of use), rather than the time of payment of the countervalue.

It also follows from the above that settlement in a foreign currency is not a requirement for the inclusion of individual transactions in the balance of payments statistics; settlement can be in the national currency, under a barter arrangement or even without compensation. Nevertheless, most balance of payments transactions are in foreign currencies and claims on and liabilities to non-residents are denominated in various currencies. The aggregation of transactions and positions in the currency of compilation requires their conversion at an appropriate exchange rate. In the case of transactions, the rate of conversion is the exchange rate used in the transaction while in the case of positions it is the exchange rate prevailing at the reference date. In respect of flows, transaction exchange rates are often unavailable; in such instances the average exchange rate for the period is generally used.

1.2 struCturE Of tHE bALANCE Of pAymENts

1. Current account 1.A Goods and services 1.B. Primary income 1.C. Secondary income 2. Capital account

2.1. Gross acquisition/disposals of non-produced, nonfinancial assets 2.2. Capital transfers

3. Financial account 3.1. Direct investment 3.2. Portfolio investment

3.3. Financial derivatives and employee stock options 3.4. Other investment

3.5. Reserve assets

The two main components of the balance of payments are the current account and the capital account together, as well as the financial account. The balancing item of the current account and the capital account is the financing capacity calculated from above (or the borrowing requirement in the case of a negative sign), while the balance of the financial account is the financing capacity/borrowing requirement calculated from below. By definition, this equals the application of the net new borrowing/

net lending; however, this equality is rarely seen in practice, owing to the peculiarities of data collection. The financing capacity calculated from above shows – together with the current account balance and the balance of the capital account – the combined balance of goods and services, income and transfers received and paid. If that is negative, it means that an external financing requirement was generated, which requires the involvement of foreign resources, if it is positive, then in an international context the country is a net creditor. The components of the financial account provide a more detailed picture about the characteristic features of this financing: what the distribution of foreign direct investment, portfolio investment, other investment is, and how reserves have changed over a particular period.

1.2.1 Current account

Current account is an important aggregate of the balance of payments, which includes goods, services, primary and secondary income.

According to the new methodology, the modified names of main categories of current account harmony with the system of national accounts has been made clear (e.g. categories of primary and secondary incomes, applied in the national accounts previously have been applied instead of the earlier categories of income, and current transfers, as well). As a result of this change, now taxes and subsidies on product and production are also recorded under primary income as opposed to BPM5, which treated them as current transfers.

Instruments of the current account (1.A+1.b+1.C) 1. Current account (1.A+1.b+1.C)

1.A.a. Goods

1.A.a.1. General merchandise on a BOP basis 1.A.a.2. Net exports of goods under merchanting 1.A.a.3. Nonmonetary gold

1.A.b. Services

1.A.b.1. Manufacturing services on physical inputs owned by others 1.A.b.2. Maintenance and repair services n.i.e.

1.A.b.3. Transport 1.A.b.4. Travel 1.A.b.5. Construction

1.A.b.6 Insurance and pension services 1.A.b.7. Financial services

1.A.b.8. Charges for the use of intellectual property not included elsewhere 1.A.b.9. Telecommunications, computer and information services

1.A.b.10. Other business services

1.A.b.11. Personal, cultural and recreational services 1.A.b.12. Government goods and services n.i.e.

1.B Primary income

1.B.1. Compensation of employees 1.B.2. Investment income

1.B.2.1. Direct investment income

1.B.2.1.1. Income on equity and investment fund shares

1.B.2.1.1.1. Dividends and income withdrawal from quasi corporations 1.B.2.1.1.2. Reinvested earnings

1.B.2.1.2. Interest

1.B.2.2. Portfolio investment

1.B.2.2.1. Investment income on equity and investment fund shares 1.B.2.2.2. Interest

1.B.2.2.2.1. Short term 1.B.2.2.2.2. Long term 1.B.2.3. Other investment 1.B.2.4. Reserve assets 1.B.3 Other primary income 1.C Secondary income

1.C.1. General government

1.C.2. Financial corporations, nonfinancial corporations, households, and HPISHs

Goods include general merchandise, net exports of goods under merchanting (in which the resident merchant purchases the goods outside the borders of the resident country, then sells them also outside the borders, without bringing them into the resident country), and the sale and purchase of nonmonetary gold, i.e. gold that is not part of international reserves. General merchandise transactions include all goods transactions between residents and non-residents that involve a change in ownership and belong to neither the other two goods categories, nor to those services that also involve movement of goods (travel, construction services, government services). This means that, in addition to simple sale and purchase transactions, factoryless production (where the principal is resident but all transactions are carried out abroad), imports of high value goods in private trade, financial leasing, goods procured by non-resident carriers in the resident country (and similarly goods procured by resident carriers abroad) and illegal transactions (smuggled goods, drugs, etc.) also form parts of this category. Although in case of financial leasing there is no change of ownership in a legal sense until the end of the lease term, in line with the economic substance of this transaction, however, when the leased goods are imported (or exported), there is an entry under goods, and, as a double entry, a financial liability (or asset) is recorded in the financial account. In the case of merchanting, acquisitions are presented as negative exports.

Goods trade in both directions is recorded at market value, on FOB terms, i.e. on exporting country’s border delivery terms (see chapter 2.1.3.4 for details on CIF and FOB parity and settlement). Those elements of the invoice value that include transport, insurance or other costs above FOB terms must be reclassified under the relevant services category.

Every real economic activity that does not belong to goods is recorded as a service. The classification of services is generally linked to the underlying activity. Exceptions to that include travel, government services and construction services, in these cases it is connected to the user of the service. These latter categories of services may also include movements of goods;

however, the main classification principle i.e. the activity itself overrides that as well.

Services also include movements of goods trade where no change of ownership occurs, even in the economic sense of the term. These transactions are manufacturing services on physical inputs owned by others (i.e. processing) and maintenance and repair services. Both must be recorded at net value. At the same time, in the case of processing those items where only the goods for processing cross the border of the resident economy and the processed goods, in the other direction, should not be reclassified under goods. Services also include assets which are results of research and development, regardless of whether one has to pay for their use only or for their ownership right (although the relevant service categories will be different). In the case of marketing assets (franchises, trademarks, logos, domain names, etc.), only charges for the use of intellectual property are classified as services; sale and purchase of ownership rights should be recorded in the capital account. Often the distinction between goods and services is difficult to draw. For example, a blank CD and a CD containing non-customised software are to be recorded as goods, while customised software belong to the category of computer and information services.

The sale and purchase of financial assets (such as loans, insurance, securities) also contain components of (indirect) services.

The seller or marketer of these products manifests in its product prices the fact that it is not only the seller (marketer), but also the service provider of these assets. These indirect services must be recorded under insurance and financial services (FISIM, i.e.

Financial Intermediation Services Indirectly Measured is a case for the latter). See Box 2 on the concept and accounting of FISIM.

The credit and deposit rates applied and actually paid by credit institutions include the effect of the intermediation fees charged by the credit institution for financial intermediation. This means that the interest payable on lending is increased by that amount, while the deposit rates paid by credit institutions are reduced by that amount compared to the reference rates of financial assets (i.e. their basic price). This financial intermediation fee, i.e. FISIM, represents the activity of financial institutions that they collect sources and then lend these to the appropriate customers, thereby providing services to non-financial institutions. Therefore, FISIM is to be recorded in the balance of payments among financial services, separately from interest.

It follows from the above definition that only the sector of financial institutions may realise revenue from FISIM and only non-financial institutions may incur fIsIm expenses. At the same time, transactions including FISIM are only recorded under other investment, because the existence of FISIM itself expresses the fact that credit institutions provide intermediation services between independent parties, free of intra-group transfer pricing and settlement prices, and by definition, other intra-group claims and liabilities do not include FISIM. There is also no recording of FISIM transactions in the case of transactions of central banks, because these are not necessarily driven by profitability, i.e. by market considerations, and in the transactions of credit institutions conducted with each other (credit institutions cannot incur FISIM expenses, therefore we can presume that their transactions conducted with one another take place at reference rates).

An example for the partition of interests into FISIM (Financial Intermediation Services Indirectly Measured) and reference interest 1. The Bank of Eden (a FISIM producer) grants a,loan to a,non-resident automotive factory (a FISIM user) in the value of 100 million farthings

with an annual interest rate of 6% (the reference rate is 5%).

2. A,non-resident automotive factory (FISIM user) places a,deposit at Bank of Eden in the value of 5 million farthings with an annual interest rate of 3% (the reference rate is 3.5%).

3. Some of the savings of the households of Eden, 3 million farthings, are placed at the non-resident Banque, with an annual interest rate of 4.5% (the reference rate is 5%).

4. The canning factory of Eden borrows 20 million farthings from non-resident Banque with an annual interest rate of 4% (the reference rate is 3.5%).

data in petak

yearly data Credits debits

fIsIm producers

1. the total actual interest of lendings by resident credit institution 6,000,000

1.a.pure interest 5,000,000

1.b. FISIM 1,000,000

2. the total actual interest of deposit placed with resident credit institution 150,000

2.a. pure interest 175,000

2.b. FISIM 25,000

fIsIm users

3. the total actual interest of the deposits placed by resident households 135,000

3.a. pure interest 150,000

3.b. FISIM 15,000

4. the total actual interest of the borrowings of the resident company 800,000

4.a. pure interest 700,000

4.b. FISIM 100,000

balance of payments yearly data Credits debits

1.A.b.7.1 FISIM 1,025,000 115,000

1.B.2.3.2. Interests (pure interests based on reference rate) 5,150,000 875,000

B.1. Deposit taking corporations except the central bank (S.122) 5,000,000 175,000

D.2. Non-financial corporations, households, and non-profit institutions serving households (S.1V) 150,000 700,000

tOtAL 6,175,000 990,000

box 2

financial Intermediation services Indirectly measured (fIsIm)

The category of travel will be identified by a new name in Hungarian from 2014. The content of the recorded items has not changed (the total value of goods and services purchased by travellers for their own use during the trip), only the Hungarian name has been altered.

primary income includes the revenues and expenditures related to the use of factors of production and financial assets, as well as taxes and subsidies on product and production.

Compensation of employees includes amounts received abroad by employees who are residents of the country compiling the balance of payments statistics or paid to non-resident employees in the compiling country, respectively. From a statistical aspect, the key issue is to determine whether an employee is to be considered resident or non-resident. With respect to natural persons, similarly to legal entities, resident status is determined based on the centre of predominant economic interest. This decision is not made on the basis of citizenship or permanent residence; instead, the key factor is the location where the natural person pursues the activity through which he/she earns a living (where he/she keeps a household). A natural person is resident in the country where he/she lives or works for a sufficient length of time, meaning at least one year for statistical purposes.

Investment income is recorded in the current account classified by form of investment. Balance of payments statistics classify investments and related incomes in a functional breakdown based on the motivation of the investor and the form of the investment.

Foreign direct investment income includes all incomes generated by foreign direct investments between residents and non- residents. The new methodology has clarified the foreign direct investment relationship, which is discussed in more detail in section 1.5.4. Income generated from loans between financial intermediaries is not part of foreign direct investment under the new methodology; these items must be recorded under portfolio or other investment. Foreign direct investment income can be split up into income of investment earned from ownership and interests earned from debt instruments. Income earned from ownership includes distributed income (dividend) and undistributed (reinvested) earnings.

Dividends are distributed earnings attributable to investors on their equity investments. Their amount is often determined as earnings per share. Income withdrawn from branches must also be recorded as dividend. At the same time, dividends of extraordinary amount, paid from retained earnings (superdividend) must be treated as a withdrawal of equity rather than as dividend, according to the recommendations of the methodology. Dividends must be recorded when the owners decide on their amount, that is, when they are declared. Equity income attributable to investors (after-tax profit, profit or loss of the corporation) is to be recorded as reinvested earnings in the balance of payments of the year when such income was actually earned. Declared dividends are deducted from the reinvested earnings of the period concerned. The treatment of after-tax corporate profits as reinvested earnings shows how direct investment affects the current account balance through income flows:

income earned on foreign investments of Hungarians increases the balance of the current account, since it is attributable to Hungarian owners, while it is reduced by income earned on investments of non-residents in Hungary, since it is attributable to non-resident owners. As a result of the method of recording, the owners’ decision on the dividend and the actual disbursement is already neutral on current account balance.

Income on debt instruments is income generated between enterprises involved in foreign direct investment relationship, by investments outside the scope of equity (such as inter-company loan, intra-group clearing account, cash pool, trade credits, etc.).

Portfolio investment income also consists of income from equity relationship and interest income related to debt securities.

Income from equity relationship includes, on the one hand, income on shares held by investors outside a company group, representing a voting power of under 10 per cent, and on the other hand, income from mutual fund shares. As regards shareholding, only dividends should be recorded, reinvested earnings should not. However, in the case of mutual fund shares both distributed and undistributed income should be recorded according to the new methodology. By definition, interest income is generated on debt securities (bonds and notes, money market paper).

Other investment income includes income on investments not classified under two previous categories, but also resulting from both equity relationships and interest incomes on debt instruments. In the case of equity relationships, the voting power outside the company group remains below 10 per cent and is non-securitised (for example, in the case of actual power under 10 per cent held in one branch), while the debt instrument exists between enterprises not in a direct investment relationship and is

also non-securitised (bank deposits, bank loans). However, intra-group debt instruments between banks and other financial intermediaries are recorded under other investments, rather than under foreign direct investments, and interest income is recorded under other investment income. Furthermore, income from other investments includes income on stocks of actuarial reserves attributed by insurance corporations to their customers.

In the case of debt instruments classified under other investment, the service component indirectly included in interest income (FISIM) should not be recorded as interest income, but rather under financial services, i.e. accrual-based interests must be adjusted by this component. This service may only be provided by a credit institution, while its user may only be an economic agent outside of the credit institution.

Under the new methodology, income on reserve assets should be recorded under a separate category (income on assets constituting part of reserves), which may also be income from equity relationship (primarily on mutual fund shares) and interest income on debt instruments.

As the balance of payments statistics are accrual-based, income should also be recorded basically on an accrual basis rather than on a cash basis. As a consequence, investment income is taken into account as accruing on a continuous basis during the term of an investment, rather than when a payment is actually made. In the case of interest, only the accrued interest not yet paid attributable to the relevant period is recorded. Until the interest is actually paid, the same amount of increase in assets or liabilities under the relevant investment instrument should be recorded in the financial account. In the case of income from equity relationships, accrual-based recording should be applied to income on foreign direct investment and income on mutual fund shares under portfolio investment (reinvested earnings).

In addition to compensation of employees and investment income, other primary income includes taxes and subsidies on product and production plus rents receivable and payable for the use or exploitation of natural resources.

secondary income includes flows related to the redistribution of income positions after real economic transactions and primary incomes, i.e. current transfers between residents and non-residents. These are transactions based not on exchange but rather on transfers between economic agents and affect disposable income. By this definition, these current transfers include taxes on income, social insurance contributions and benefits, aids and insurance premiums, current transfers of private individuals and various organisations, benefits payable to or received from international organisations, etc.

1.2.2 Capital account

2. Capital account (2.1+2.2)

2.1. Gross acquisitions/disposals of non-produced, nonfinancial assets 2.2. Capital transfers

Capital account includes acquisition and disposal of non-produced and nonfinancial assets plus capital transfers receivable and payable between residents and non-residents.

Transactions of non-produced, nonfinancial assets show acquisition and disposal of ownership rights of non-produced and nonfinancial assets. The scope of these goods includes the marketable exploitation rights of natural assets, marketing and other marketable assets (such as goodwill, contracts, licences, etc.). As discussed earlier, any transactions on intellectual properties related to produced assets is recorded under services, and fees related to the use of non-produced and nonfinancial assets are recorded partly under services, partly as primary income.

In contrast to secondary income, capital transfers are such transfers that do not affect the disposable income, but rather the disposable nonfinancial or financial assets. They may be transfers provided in kind or in money and cover wide areas: investment grants, transfer of title to capital assets, debt forgiveness, etc., but the payment of contribution to international organisations also belongs to this category.

1.2.3 financial account

3. Financial account (3.1+3.2+3.3+3.4+3.5) 3.1. Direct investment

3.1.k. Direct investment (Assets) 3.1.1.k. Equity

3.1.1.1.k. Equity other than reinvestment of earnings 3.1.1.2.k. Reinvestment of earnings

3.1.2.k. Debt instruments 3.1.t. Direct investment (Liabilities) 3.1.1.t. Equity

3.1.1.1.t. Equity other than reinvestment of earnings 3.1.1.2.t. Reinvestment of earnings

3.1.2.t. Debt instruments 3.2. Portfolio investment 3.2.k Assets

3.2.1.k Equity and investment fund shares 3.2.1.1.k Equity securities

3.2.1.2.k Investment fund shares 3.2.2.k Debt securities

3.2.2.1.k Short-term debt securities 3.2.2.2.k Long-term debt securities 3.2.t Liabilities

3.2.1.t Equity and investment fund shares 3.2.1.1.t Equity securities

3.2.1.2.t. Investment fund shares 3.2.2.t Debt securities

3.2.2.1.t Short-term debt securities 3.2.2.2.t Long-term debt securities

3.3. Financial derivatives and employee stock options 3.3.k. Assets

3.3.t. Liabilities 3.4. Other investment 3.4.k Assets

3.4.k.r. Short-term debt 3.4.k.h. Long-term debt 3.4.1.k Other equity

3.4.2.k Currency and deposits 3.4.3.k Loans

3.4.4.k Insurance, pension schemes, and standardised guarantee schemes 3.4.5.k Trade credits and advances

3.4.6.k Other accounts receivable 3.4.t Liabilities

3.4.t.r. Short-term debt 3.4.t.h. Long-term debt 3.4.1.t Other equity

3.4.2.t Currency and deposits 3.4.3.t Loans

3.4.4.t Insurance, pension schemes, and standardised guarantee schemes 3.4.5.t Trade credits and advances

3.4.6.t Other accounts payable 3.4.7.t SDRs

3.5.c Reserve assets 3.5.1.k. Monetary gold 3.5.2.k. SDRs

3.5.3.k. Reserve position in the International Monetary Fund (RPF) 3.5.4.k. Currency and deposits

3.5.5.k. Securities

3.5.6.k. Other reserve assets

The financial account shows changes in financial assets and liabilities generated by transactions between residents and non- residents. The balance of these items, the net lending/net borrowing, theoretically equals the aggregate balance of current and capital accounts, in other words, the net financing capacity to non-residents. For example, if the net financing capability to non-residents is positive according to the balance of current capital accounts, then the resident economy has the same net financing capacity to non-residents upon financial account.

The classification of investments is based primarily on the motivation of investors and the form of investment in financial account. Accordingly, financial account includes the following functional categories: direct investment, portfolio investment, financial derivatives and employee stock options, other investment and reserve assets of the monetary authority. Within each category the primary breakdown is separation between assets and liabilities, and within that there are additional instruments.

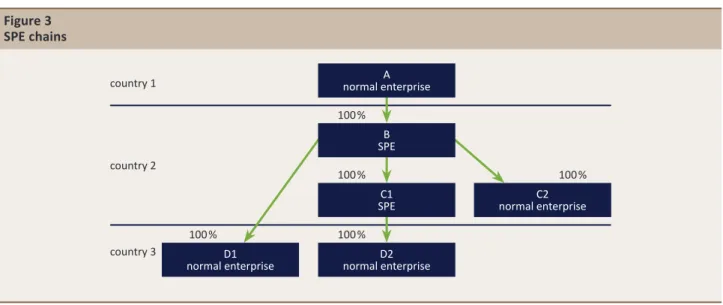

foreign direct investment includes those foreign investments where an investor resident in one country obtains long-term control or a significant degree of influence over a company resident in another country. The size and form of foreign direct investment is primarily determined by long-term strategic plans and ownership considerations, which often optimise investment and financing decisions on the level of an entire multinational company group. Long-term control or influence refers to the time horizon of the investment on the one hand and to the effective influence on the management of the enterprise established through the investment on the other hand. One of the important changes in the new methodology is a clearer, precise definition of the framework of the direct investment relationship. In that framework, the definition of an investment chain is based on the clarification of the role of control (over 50% of the votes) and influence (10% to 50% of the votes), as well as on the relationship with fellow enterprises (under 10% of the votes). The rate of voting power, as opposed to the rate of ownership, has become the criterion of the relationship. The framework also covers links between ownership chains. If one or more ownership chains originate from one investor, every enterprise in every chain is in a direct investment relationship with each other. The new methodology gives significantly greater emphasis to the recording of transactions and positions between fellow enterprises. There is more focus on the analysis of the balance sheet data of the company. Most of the changes are manifested in the presentation of data with more detailed and new breakdowns (e.g. by the presentation transactions/positions under equity in direct investment enterprises, reverse investment [an equity of under 10% in the parent company] and between fellow enterprises). The breakdown by assets and liabilities has been inserted into the standard presentation of the balance of payments statistics, while the presentation by directional principle has become supplementary.

Transactions affecting the ownership rate or the investment relationship may appear in two forms: as the reinvestment of income from the normal operating surplus of a direct investment enterprise, and as other transactions (such as purchase of shares, disinvestment, declaration of a superdividend,1 etc.).

Debt and other financing relationships besides equity relationships between the direct investor and the direct investment and those between fellow enterprises should also be recorded under foreign direct investments. These are fundamentally debt financial instruments, although they do not necessarily provide a long-term financing source. Their classification under foreign direct investments is justified by the fact that these economic agents are not independent enterprises, rather having a direct

1 If a dividend, which the company pays to its shareholders, is outstandingly high or higher than the normal operating surplus in the relevant period, under the BPM6 methodology, it should be recorded not as a dividend (current account), rather as disinvestment called a superdividend (financial account).

investment relationship with each other, therefore transactions between these parties may be subject to conditions other than fair market conditions. These transactions include loans between these enterprises, assets and liabilities due to dividends declared and paid, assets and liabilities resulting from cash pool and intercompany accounts, intragroup trade credits, debt securities as well as other assets and liabilities and should be recorded under debt instruments.

Portfolio investment also includes equity and debt instruments. Equity includes holding of shares representing voting power of under 10 per cent and mutual fund shares. Here, reinvested income should only be recorded under mutual fund shares. Debt instruments cover securitised credit relationships (bonds and money market instruments). Debt securities should be classified according to their original maturities.

Portfolio investment is characteristic of the largely anonymous relationship between the issuers and holders and the high degree of trading liquidity in the instruments recorded under this category.

Financial derivatives and employee stock options include the trading or realisation of a risk related to changes in price of a financial or nonfinancial instrument which itself becomes a separate financial asset. Transactions under derivatives may be recorded at any point of these deals and cannot be classified under either equity or debt instruments.

Financial derivatives are classified into two main categories: forward-type derivatives including swaps and option-type derivatives.

In a forward-type contract the parties agree to exchange a specified quantity of an underlying item (real or financial) at an agreed price on a specified date. In certain swap contracts, the parties agree to exchange cash flows the values of which are based on the deviation from reference prices (interest rate or exchange rate) calculated in accordance with prearranged terms.

At its inception, a forward type contract usually has zero value. This includes interest rate swaps, forward rate agreements (and various foreign exchange forward agreements). In an option-type derivative, in return for the payment of an option premium, the purchaser of the option acquires the right but not the obligation from the writer of the option to sell (put option) or buy (call option) a specified real or financial asset on or before a specified date. At its inception, the value of the option is equal to the premium specified in the contract (generally but not necessarily equal to the premium actually paid upon contracting).

The significant difference between forward-type and option-type derivatives is that in the former case either party can be on the creditor or debtor side depending on changes in the price of the underlying item, while in the case of an option, the writer remains on the debtor and the buyer remains on the creditor side throughout the life of the contract.

In contrast with the above option, employee stock options do not have their own markets; they should rather be considered as a benefit provided by the employer. However, similarly to financial derivatives, their assessment and realisation depends on the development of the price of the underlying (usually financial) product.

Other investment includes investments not recorded under foreign direct investments and portfolio investments (also excluding foreign reserves which should be treated specially). These investments also include other equity and debt instruments. Non- securitised equity relationships with a voting power of less than 10 per cent should be recorded under other equity. Debt instruments include, among others, trade credits outside the company group, interbank loans, syndicated loans and currency and deposit transactions which are not recorded under international reserve assets. In the case of loans, maturity should be determined according to the remaining maturity. Assets and liabilities of banks and other financial intermediaries on/to their parents and subsidiaries should be included under other investment, rather than under direct investment.

Other investment includes debt vis-à-vis the IMF owing to SDR allocation through member states, indicating that SDR allocation recorded under international reserve assets means liabilities of the resident economy as well.

International reserve assets have key importance in the balance of payments and in the analysis of the external position. In the balance of payments methodology, reserve assets are liquid assets vis-à-vis non-residents controlled by and readily available to monetary authorities. These assets can be used directly to make payments in the case of payment difficulties, indirectly to ease financial pressure by intervention on foreign exchange markets to affect the currency exchange rate or for any other purposes.

However, as demonstrated by the example of SDR, liabilities may be linked to the international reserve assets in other parts of the balance of payments, and these liabilities related to international reserve assets should be presented as supplementary information.

1.3 INtErNAtIONAL INvEstmENt pOsItION

3.1. Direct investment

3.1.1. Equity and investment fund shares

3.1.1.1. Direct investor in direct investment enterprises

3.1.1.2. Direct investment enterprises in direct investor (reverse investment) 3.1.1.3. Between fellow enterprises

3.1.2. Debt instruments

3.1.2.1. Direct investor in direct investment enterprises

3.1.2.2. Direct investment enterprises in direct investor (reverse investment) 3.1.2.3. Between fellow enterprises

3.2. Portfolio investment

3.2.1. Equity and investment fund shares 3.2.1.1. Equity securities

3.2.1.2. Investment fund shares 3.2.2. Debt securities

3.2.2.1. Short-term 3.2.2.2. Long-term

3.3. Financial derivatives and employee stock options 3.4. Other investment

3.4.1. Other equity

3.4.2. Currency and deposits 3.4.3. Loans

3.4.4. Insurance, pension and standardised guarantee schemes 3.4.5. Trade credits and advances

3.4.6. Other accounts receivable/payable 3.4.7. SDRs

3.5. Reserve assets 3.5.1. Monetary gold 3.5.2. SDRs

3.5.3. Reserve position in the International Monetary Fund (RPF) 3.5.4. Currency and deposits

3.5.5. Securities

3.5.6. Other reserve assets

The flow-based balance of payments statistics are closely linked with the stock-based statistics on the international investment position. These two sets of statistics provide for a coherent recording of the transactions and positions of an economy vis-à-vis the rest of the world. International investment position shows at a certain point in time the value and composition of the stock of financial assets and liabilities of an economy vis-à-vis non-residents as well as components of changes since the previous period. The classification of the international investment position by financial instruments is identical to the classification of the financial account in the balance of payments and corresponds to the investment income categories in the current account. This assures the reconciliation of flow and stock data and the consistent accounting for the earnings on various investment categories.

The difference between the two sides of the balance sheet, i.e. assets and liabilities, represents an economy’s net position (net assets or liabilities) vis-à-vis non-residents, which equals the country’s net worth resulting from financial investments vis-à-vis the rest of the world. Calculating without equity securities, equity investment and financial derivatives, this difference yields the net international creditor or debtor position.

In economic terms, liabilities and debt are not synonymous. According to the generally accepted definition, gross external debt includes those debts (obligations) of a country’s residents vis-à-vis another country’s residents that involve a repayment obligation (with or without the payment of interest) or, conversely, an interest payment obligation (with or without principal payment). Under this definition, equity investments are not considered debt, irrespective of recording them under foreign direct investments, portfolio investments or other investments. In addition, financial derivatives are also not considered debt based on this definition because at their inception there is no transfer of funds related to the instruments that would need to be repaid at a later date (no repayment obligation), and no interest accrues on them. The purpose of financial derivatives is not to provide funding to economic entities, but to facilitate risk management and risk trading. Financing with financial instruments linked with various types of equity and transactions with financial derivatives do not affect the country’s net external debt, and therefore they are referred to as non-debt generating financing.

Between two points in time, changes in the stock are driven by (1) transactions shown in the financial account of the balance of payments, (2) revaluation (exchange rate changes, price changes), and (3) other changes in volume (e.g. write-offs). The value of stocks since may vary for reasons other than transactions or revaluation, including debt write-offs. Reclassification of certain items from one instrument to another to assure compliance with changed classification criteria should also be considered as other changes in stock. This occurs, for instance, when the 10 per cent threshold between direct investment and portfolio equity investment is exceeded. If an investor who was below this threshold in the previous period, makes additional investments and exceeds the limit in the next period, the transaction carried out in the reference period should be recorded under direct investment in the financial account (although retrospective adjustment is not required), whereas in the IIP, the stock recorded under portfolio investment in the preceding period should be reclassified as direct investment. Such reclassifications should be recorded under other changes in volume.

1.4 bALANCE Of pAymENts IN tHE mACrOECONOmIC stAtIstICs frAmEwOrK, LINKs tO tHE systEm Of NAtIONAL ACCOuNts

This chapter explains how the balance of payments and the related international investment position form an integral and organic part of the broader system of national accounts.

The UN System of National Accounts (SNA), which is one of the most significant contributions of the 20th century to expanding the toolset of economic analysis, is the international set of standards that renders comparable the economic output of the individual countries through the system of national accounts of the various countries. The role of national accounts is to document the economic flows of a country in an integrated and consistent system. They cover aspects of the output of manufacturing and services, income creation and distribution, consumption and accumulation.

National accounts constitute a self-contained system of accounts presenting the macroeconomy through their interrelated and integrated accounts and statements. The system of national accounts consists of production accounts, accumulation accounts and balance sheets. The System of National Accounts draws up these accounts for the following sectors: resident sectors:

within that nonfinancial corporations, financial corporations, general government, households, non-profit institutions serving households and non-residents, i.e. the rest of the world. The aggregation of these sectors shows the production, income and accumulation trends and the net worth of the total economy.

In combination, the balance of payments statistics and the related international investment position provide for the coherent recording of the transactions and positions of an economy vis-à-vis the rest of the world. It essentially corresponds to the rest of the world sector account in the system of national accounts with the exception that while balance of payments statistics present the transactions, assets and liabilities of resident economic sectors vis-à-vis the rest of the world, the rest of the world account looks at the same elements from the perspective of non-residents. In English, the balance of payments and the international investment position are referred to as International Accounts.

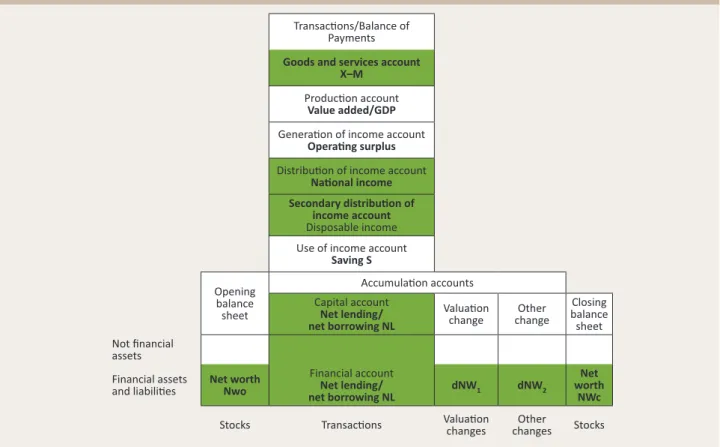

Figure 2 presents the System of National Accounts. Accounts which have their counterparts in the BOP and IIP statistics are highlighted, and the balancing items of the various accounts are indicated in bold.

relationships between national account aggregates and the balance of payments

On the production account of national accounts resources and uses are in equilibrium. This means an equilibrium between gross output and imports of goods and services on the one hand, and final and intermediate consumption, capital formation and export of goods and services on the other hand. Gross domestic product (GDP) is one of the most extensively used measures of economic performance defined as the difference of gross output and intermediate consumption (value added). At the same time, this measure is also an income category as it expresses a volume of income identical to the production measured. GDP does not contain income from abroad: it measures the income produced by the residents of a country, rather than the location where such income is earned. If the value of GDP is adjusted for the balance on primary income (BPI), the gross national income (GNI) is obtained.

If we focus on transactions involving the rest of the world, i.e. add to the net exports of goods and services the balance of primary and secondary income (net current transfers) with non-residents, we arrive at the current account balance (CAB).

figure 2

Overview of the key accounts and balancing items of the system of National Accounts as a framework for macroeconomic statistics including International Accounts

Transactions/Balance of Payments goods and services account

X–m Production account

value added/gdp Generation of income account

Operating surplus Distribution of income account

National income Secondary distribution of

income account Disposable income Use of income account

saving s Opening

balance sheet

Accumulation accounts Capital account

Net lending/

net borrowing NL

Valuation

change Other change

Closing balance sheet Not financial

assets

Financial account Net lending/

net borrowing NL Financial assets

and liabilities Net worth

Nwo dNw1 dNw2 Net

worth Nwc

Stocks Transactions Valuation

changes Other

changes Stocks where the components relating to the BOP and IIP are highlighted and the name of the balancing item is indicated in bold.

gdp = gross domestic product s = gross saving

NL = net lending

NwO = opening level of net worth NwC = closing level of net worth

dNw1 = change in net worth from revaluation

dNw2 = change in net worth from other change in volume

Correlations between national account aggregates and the balance of payments

Resource = Use (1a)

GO + M = C + G + I + X + IC (1b)

GDP = GO - IC (2a)

= C + G + I + (X - M) (2b)

GNI = GDP + BPI (3)

GNDI = GDP + BPI + BSI (4a)

= C + G + I + (X - M) + BPI + BSI (4b)

= C + G + I + CAB (4c)

CAB = (X - M) + BPI + BSI (5a)

= GNDI - (C + G + I) = GNDI - A (5b)

S = GNDI - C - G (6a)

= I + CAB (6b)

CAB = S - I (7a)

= (SH - IH) + (SE - IE) + (SG - IG) (7b)

KAB = NKT - NPNNA (8)

CAB + KAB = S - I + NKT - NPNNA = NFI (9)

gO = gross output

IC = intermediate consumption

C = private consumption (household consumption) CAb = current account balance

g = government consumption gdp = gross domestic product gNI = gross national income A = domestic absorption

gNdI = gross national disposable income I = gross domestic (nonfinancial) investment m = import of goods and services

bsI = balance on secondary income

NfI = net foreign (financial) investment (or net lending vis-à-vis the rest of the world) NKt = net capital transfers from abroad

NpNNA = net purchases of non-produced, nonfinancial assets KAb = capital account balance

bpI = balance on primary income s =gross saving

X = export of goods and services

(SH-IH) = net financial saving by households (SE-IE) = net financial saving by corporations (SG-IG) = net financial saving by government

The current account balance reflects the economy’s saving position vis-à-vis the rest of the world (7a); in other words, whether the value of gross saving relative to gross investment results in net external borrowing (current account deficit) or lending (current account surplus).

Any amount of the disposable income not used within an economy is automatically recorded in the balance of payments as funds allocated abroad and any domestic use in excess of the disposable income is recorded as borrowing (5b). In order to establish if an economy was a net lender or a net borrower in a specific period, the aggregate balance of the current and capital accounts is needed (9). The relationship between the net financial positions of the individual sectors and the current account balance is shown in equation (7b).

These equations express necessarily fulfilled identities following from the accounting principles rather than rules of conduct.

Consequently, in themselves they are insufficient for the description of causality between macroeconomic aggregates. The establishment of causality between these variables is within the realm of economic analysis. However, by their very nature,