Business Planning

/Practical Workbook/

Business Planning

/Practical Workbook/

Written by:

Tibor Pupos

Pannon University Georgikon Faculty Győző Demeter

Pannon University Georgikon Faculty Edited by:

Tibor Pupos Reviewed by:

István Takács

Károly Róbert University College Transleted by:

Judit Poór

University of Debrecen, Centre for Agricultural and Applied Economic Sciences • Debrecen, 2013

© Tibor Pupos, 2013

Manuscript completed on: 31. Auguszt 2013.

University of Debrecen Faculty of Applied Economics and Rural

Development

Pannon University Georgikon Faculty

ISBN 978-615-5183-90-4

UNIVERSITY OF DEBRECEN CENTRE FOR AGRICULTURAL AND APPLIED ECONOMIC SCIENCES

This publication is supported by the project numbered TÁMOP-4.1.2.A/1-11/1-2011-0029.

Contents

Foreword 5

1 The place of the business plan in the system of the planning, the process of its making

6

2 The content elements of the business plan 8

3 The making of the business plan 13

3.1 The presentation of MODEL Ltd, its status data 13

3.2 The making of the sales plan 20

3.3 The content and the making of the production plan 24

3.4 The planning of the resources 31

3.4.1 The planning of the current assets as resources functioning as working capital

39 3.5 The content and the process of the making of the financial plan 42

3.5.1 The planning of the income from sales 43

3.5.1.1 The income from sales and other incomes of cultivation 43

3.5.1.2 The income from sales of the service 44

3.5.1.3 The income from sales and other incomes of dairy-farm 44

3.5.2 The planning of the production expenses 44

3.5.2.1 The planning of the expenses of the cultivation 47 3.5.2.2 The planning of the expenses of the service 51 3.5.2.3 The planning of the dairy-farm's expenses 54 3.5.3 The planning of the expenses of the expense places 58

3.5.3.1 The planning of the expenses of the assistant firm services

58 3.5.3.2 The planning of the general expenses of the cultivation 59 3.5.3.3 The planning of the expenses of the central

administration

59

3.5.4 The money currents of the function 63

3.5.5. The money circulation plan 68

3.5.5 The planning of the result 73

3.5.6 The source demand and source structure 76

3.5.7 The making of the balance plan 77

3.5.8 The cash flow plan 79

3.5.9 The plan of other financial information 86

The register of sources 93

Appendix 94

Foreword

The body of knowledge of the business plan is one of the most important subjects in MSc training. The authors do not wish to prove this since students will have an occasion richly to make sure from this direction. After all, why is it so? Responding to the question it is necessary to take an important viewpoint into consideration that to meet to the requirements of the economic agricultural engineer, the acquisition of the body of knowledge on skill level, the development of the competences being connected to these, cannot be imagined without independent and team work of the students. The completion of a business plan provides a distinguished opportunity to the fulfilment of these requirements. The use of the elemental knowledge to the solution of a single given problem means the largest difficulty. This presupposes the existence of the problem recogniser and the synthetising ability. To the development of this the tasks of the practical occupations of the subject, the completion of the business plan of the Model Ltd creates an opportunity. At the compilation of the curriculum – to the aim of meeting the requirements expressed against the students, the development of the related competences – the central question was how to teach. We drew up the body of knowledge to be acquired, taking the undermentioned viewpoints into consideration:

we differentiated the body of knowledge to be taught fundamentally not horizontally, but vertically – that is in its depth – we laid the emphasis onto the causal connections and on their exploration;

the independent student working receives an important role, work is to be solved differentiated, partly individual, partly in team work;

we insure the student’s independent working based on case studies;

we try to give an opportunity to the students to let the independent works be outlined in the framework of an independent lecture, joined to a presentation.

The viewpoints and principles mentioned above drew that margin and frameworks we marked off the body of knowledge of the note, and we fixed the methods of the teaching of the body of knowledge. Since there is no need for a new body of knowledge fundamentally, we allude to the related body of knowledge and the theoretical note only in a concrete case at each planning tasks. (The answers to question of what? why? and how? and the detailed exploration of the causal connections can be found in the algorithm of the business plan). The processing of the body of knowledge happens on practical lessons, with teacher management.

The business plan is needed to be prepared in team work independently, to be handed in for a given deadline and to be protected in the framework of a presentation according to the given content and formal requirements. The algorithm of the development and the worksheet of each content elements of the business plan stand for the students' provision. (These can be found in the enclosure, indicating the maximum extent of the task in a concrete case that cannot be exceeded.) The difference in the supposed and the actual activity of the students and the mood to independent work, etc. may cause an essential difference between the sketched concept and the realisation and this may yield to that we reshape our concept later.

The insurance of the expected efficiency presupposes that all of the elements are needed to be on the expected standard. We wait for the active attitude of students to independent work, the honest criticism and the positive and negative remarks equally. The entire realisation of the aims presupposes real team work because of this we wish a good work to all of the concerned.

Keszthely, 30th November 2012.

the Authors

1. The place of the business plan in the system of the planning, the process of its making

It is not possible to miss that action program with an economic character that implies the ideas concerning the company's future, the strategic aims to a longer distance in the interest of fruitful adaptation to the changes of the environment because of the interactions between the company and environment. The making in a written form of this action program is the business plan. So, the business plan is the company's worked out action program of the realisation of the strategic aim to an actual time frame. It comes into existence as the result of the business plan process, when they are fixed to the given time frame (at most 5 years) in a quantified and text form:

the aims to be achieved,

the tasks to be solved,

the external and internal resources necessary to the realisation,

the external and internal opportunities of the realisation and

the expected result.

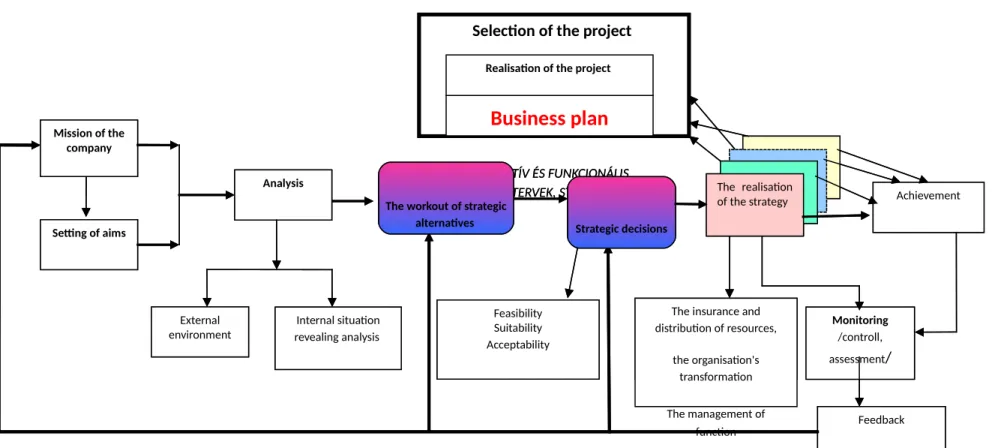

Figure 1. exemplifies the place of the business plan in the system of the strategic plan. Based on the figure it is visible, that the content of the business plan finally concerns to the concrete project serving the achievement of the strategic aim. The strategic aim was drawn up on the other hand embedded in the company's narrower and wider environment. We use the concept of the business plan in that sense in the following, when its completion and content serves the realisation of the strategic aim and external resources are needed (support, credit).

Known, that we can make the business plan for different aims. Reasonable, that the content of the business plan, its detail and the requirements expressed against the business plan are different according to the related aims. The detail of business plans may be deeper prepared for the own aim, or on the contrary, it depends what is required or what is necessary to handle pointedly. It is necessary to put the emphasis somewhere else if a stranger (banking or application specialist judging our loan application) is a reader, it is necessary to make it understandable for him, and to convince him about the vocational tenability of our strategic aims and its profitability. The representation and the form of the plan cannot be neglected in the case of a business plan made for the exterior affected. That representation is expedient that is sympathic to the reader and shows fastidiousness. As an important viewpoint it is expedient to take into consideration that it is necessary to making the business plan in such a way to fit for that purpose, who we prepare it for.

The common point of the business plans for the different purposes can be marked in their content parts. The content parts so carry fundamentally the same information, but they are worked off differentiated, between different formal frameworks and with a different detail depending on the aim. The business plan is not only a forecast, but an action plan or an action program too. It is important to follow the realisation of the business plan with attention continuously, it is necessary to reveal the reason behind the differences and to do the necessary modifications if it is needed and to fix to the changed circumstances.

Figure 1. The process of the strategic plan: the place of the business plan in the system of the strategic plan

Source: Own work of author Projekt/ek/ kiválasztása

Erőforrások biztosítása és elosztása, Szervezet átalakítása

Működés irányítása A vállalat

küldetése

Célok kitűzése

Elemezés

Külső környezet

Belső, helyzetfel-táró elemzés

Stratégia megvaló-sítása Projektek megvalósítása

Üzleti terv

/OPERATÍV ÉS FUNKCIONÁLIS

TERVEK, STB./ Teljesítmény

Megvalósíthatóság Alkalmasság Elfogadhatóság

Monitoring/Ellen őrzés, értékelés/

Visszacsatolás Stratégiai döntések

Stratégiai alternatívák kidolgozása

Selection of the project

The insurance and distribution of resources,

the organisation's transformation The management of

function Mission of the

company

Setting of aims

Analysis

External environment

Internal situation revealing analysis

The realisation of the strategy Realisation of the project

Business plan

/OPERATÍV ÉS FUNKCIONÁLIS

TERVEK, STB./ Achievement

Feasibility Suitability Acceptability

Monitoring /controll, assessment/

Feedback Strategic decisions

The workout of strategic alternatives

2. The content elements of the business plan

There is not an obligatory scheme to the content, extent and construction of the business plan as we already related in the previous chapter. The aim of the making and the claim, who it prepared for are normatives. According to Bocsó et.al (1999) the content of the business plan has to give an answer to the undermentioned questions:

where the company starts from in the time of the plan making,

what kind of conditions does it have,

where, under in much time and why wants to get,

the what kind of result of the realisation of aims will be formulated in a business plan,

how and what kind of device and resource can be reached the set aim with.

If the aim of the business plan is the withdrawal of exterior sources, the questions to be responded are the following:

what aims serves the external resource,

what kind of the market opportunities,

how the use of the resources happens,

how the conditions being attached to the return develop,

what kind of ideas there are to parry the adverse changes of the environment.

The answers sketched in the previously define the content parts of the business plan fundamentally. These content parts will have different emphasis, in accordance with the function of the business plan. It is reasonable, that the quality and the market situation of the product, the modernity of the production technology, etc. for example for an investor can be treated as an important question, so the knowledge of the main elements of the corporate strategy has priority. The financial institution offering the credit on the other hand puts the conditions of return and the establishment of the financial position forward not left out of consideration the viewpoints listed previously. It is necessary to mention the company's size, its market position, the market's character and the conditions of the market as the factors influencing the complexity of the business plan. The construction of the business plan may be so a very diverse one. We write the related body of knowledge through a possible business plan. Sketchily we review the main content elements of the business plan concentrating on the essential content questions based on the sources being attached to the topic (Bocsó et.al 1999.; Gyulai-Kresalek, 2002).

The business plan can be itemized to the undermentioned main content parts:

1. Introduction

2. Managerial summary

3. Product chain analysis (his previous draughting: Industrial branch analysis (background analysis))

4. The presentation (description) of the company 5. Function plan (Production plan)

6. Marketing plan 7. Organizational plan

8. The presentation of the resource demand and resource structure 9. Financial plan

1. Introduction

The most important data concerning the company, the name of the company, short summary, address, telephone, fax number, the owners’ name, the sharing proportions of them, their address, phone number, the data of the management, the year of the foundation of the company (registration), short historical presentation, the field of activity of the company (character), the capital, credit and function money demand of the company, the confidential treatment claim concerning the plan.

2. Managerial summary

It is expedient to prepare this part after the development all of the elements of the complex business plan. It gives the synthesis of a business plan. It highlights the most important questions relevantly to the future tersely, getting to the point, extending to all parts of the business plan, the planned financing method, the conditions concerning the financial position, etc.

3. Product chain analysis (his previous draughting: Industrial branch analysis (background analysis))

It is known that the company is in a strong connection equally with its narrower and wider environment. For the company so it may not be indifferent what kind of competitors he has to compete. The product chain analysis aims at how the market of the product chain develops regarding the future. Responding to the question may happen with the help of a complex analysis only; it has to expand on the examination of all of the related questions.

The undermentioned ones may be the main viewpoints of the making of the analysis:

the main features of the product chain (the presentation of the development, the presentation of the dynamics, its trend, the competitors, the market's segmentation, the situation of the new product, the vision of connecting to and leaving the market, etc.)

4. The presentation (description) of the company

The aim of the chapter is the presentation of the company so detailed, which makes it clear what the company's scope of activity, how the efficiency of its management is, and what the planned project concerns to. The content dissection of the chapter can be prepared according to the undermentioned ones:

The data concerning the company (Appendix 1.)

a/ Basic data: The company's name, address, legal status

b/ The proprietors' data: The proprietors' name, address, the ownership ratios of each proprietor

c/ The data of the employed: numbers of employees and physical employees, number of full and part time employed staff

d/ Financial information about the company: the communication of the income statement, the resource formation, balance sheet, the related important financial indices relevantly for the last three years.

The presentation of the company's business activity:

This part implies the description of the company's products and services. It is necessary to present the functional features (advantages, disadvantages) of services and products in detail. It is necessary to formulate these features examined from the viewpoint of the consumer.

5. Function plan (production plan)

This content element of business plan implies the presentation of production process of the products and services. The elaboration of the presentation of the production process has to be an important decision viewpoint. The content depends on the function (activity) of the company being commercial or a producer. If the company is a producer, the plan part is the production plan and in the case of a company making a service activity or if it is a commercial one, we call it a service or commercial plan. These plans also do not have a scheme accepted universally. Depending on the activity the main content elements may be the following:

(A) In case of production plan:

The presentation of the production process:

the used production methods,

necessary resources (machines, equipments, workforce),

the purchase of inputs (the names of the important suppliers),

the establishment of the expenses of the production,

the capacities standing for provision,

future resource claim,

innovational programs (licences, know how) The presentation of the important sub-contractors (B) In case of service or commercial plan:

the type of the merchandise purchase,

the applied stockpiling system,

the necessary supply levels, the expenses of them,

the record system of the orders,

the applied logistic system,

the review of the packing and packaging type of the sold commodity.

6. Marketing plan

Universally accepted, that the marketing plan – beside the financial plan – is the most important part of the business plan. The aim is that what kind of marketing strategy we wish to achieve the planned result with. This part presents the results of the analysis concerning the market situation according to this, and it also presents the worked out marketing plan based on this. The main content elements of the plan may be the undermentioned ones:

a/ The characterisation of the market and the opportunities:

It implies the expected demand, the aim markets, the features of the market segments and their significance from the viewpoint of the company.

b/ The presentation of the external factors and the competitors:

It is necessary to go into detail about the review of the exterior factors influencing the development of the results mostly in this part. It is necessary to treat emphasised the most important competitors, the competitors' positions, their strong and weak points, their market share, as one of the most important risk factors.

c/ The presentation of the marketing stategy of the company:

In the content part it is necessary to summarize how the company wishes to apply

d/ The sales forecast:

It is necessary to concretize the planned increase of the sales revenues in this part.

Above this, it is necessary to go into detail about the change of the market share broken down according to product line and consumer groups.

e/ Additional information:

It is expedient to attach so additional materials to the marketing plan, which support the previously sketched ones, for example: the supplier contracts, branch studies, etc.

7. Organizational plan

The company form and the form of ownership have to be treated as an important factor in terms of the company's fruitful function, what is the determining element of the company's leadership organization system too. It is expedient to give the information concerning the organizational form in a text and organogram form. In a text form it is expedient to sketch the decision levels, the under and upper relations, and the viewpoints of the sharing of the related work and responsibility. It is necessary to assess the leadership organization system, if it is in harmony with the aims, what kind of guarantees gives to the realisation of the strategic aims and to the company's fruitful function. It is necessary to go into detail about the company's personnel politics and its strategy that is it is necessary to deal with the employees' selection, with the training and its professional development, the interest and incentive system applied at the company. The organizational plan so has to imply information that show who directs and in what kind of organizational form the company unambiguously and it has to come out that what the human resource strategy of the company is like.

8. The presentation of the resource aim and resource structure

It implies the presentation of the sum of the planned resource demand and its structure in detailed for the indication of the credit conditions and planned money currents.

9. Financial plan

It constitutes the essential part of the business plan. It implies the presentation of the objectives with a financial-economic viewpoint. It is partly used for summarize the previous chapters, partly for its supplement from a financial viewpoint. It gives information about the yield; it is possible to count on for the potential investors in case of the investment to the company. The financial part of the business plan gives information for the creditors about how much is assured the tenability and continuity of interest payment. Its content dissection can be the following:

Cost and income plan;

Liquidity plan;

Balance sheet plan;

Cash flow plan;

Other financial information (break-even point analysing, indices presenting the financial position etc.).

10. Risk management

An important requirement of the business plan is to be real and convincing. It belongs to this that the company is necessary to recognise those risk factors and potential sources of danger, with which the company has to count on the road leading to the achievement of the aims. It is possible to formulate and work that strategy only with the knowledge of these, with which

adverse effects can be moderated for the company. The essential content element of the plan part is the listing of the related risk factors, and the delineation of the exemplary act alternative.

The risk elements may be diverse. A starting company has to reckon with other risk elements (the insurance of clientele, getting in to a market etc.), than that one which is working for a long time. It is easily reasonable that a well-funded big company's opportunities entirely other, than a less well-funded small enterprise's.

11. Appendix

General practice, that we refer to documents, which are placed in the appendix, in the given part of the business plan. These documents support the favourable judgement of the business plan and help

in the tenability of the plan, the company's economic situation and each text parts (foe example the company's most important financial statements onto the previous 2-3 years, SWOT analysis

concerning the company, the vocational curriculum vitae of the leaders, etc.).

3. The making of the business plan

3.1. The presentation of MODEL Ltd, its status data

MODEL Ltd can be found in Pearl micro-region. In the case study the conditions and the operative program of the micro-region are known, the generated projects are known.

MODEL Ltd wishes to develop and modernize his growing technologies fixed into the related strategic plans. The owners of MODEL Ltd want to accomplish a considerable development since an increasing claim comes forward the precision technologies sparing the environment and the local dairy products. This development affects two areas:

The application of precision technology, the satisfaction of the claim coming forward in the micro-region.

The development of presently the livestock of 35 pieces of cow and their progeny in a 50 room dairy-farm settlements until the settlement's capacity.

MODEL Ltd dealt only with cultivation until now. The standard of the growing technologies can be considered most modern one in the area. The Ltd.organized vocational shows several times. The instrument supply is satisfactory to the vocational viewpoints maximally from all viewpoints. The nutrient provider ability of the soil is good and it creates the opportunity to the application of the precision technologies as the result of the practice of the previous years.

The related soil survey results, the nutrient map of the boards and the yield maps stand for a provision. The conditions of the introduction of the precision technologies are given on the area of the plant protection. It is managed to insure this with a application source, which they won in the last year. Regarding the future the claim of the agricultural companies of the micro-region can be treated as an important viewpoint onto the use of the precision plant protection technologies service. Some 3050 ha of cumulative claim comes forward based on the related survey, for the precision plant protection service. The maximum price of the service can be 3300 Ft/ha. The customers would not take advantage of the service at a higher price based on the results of the survey.

Because of the change of the family relationships – the elder boy got married and his wife inherited the dairy-farm settlement, which got into his possession of MODEL Ltd 50 pieces of cow and his progeny are the settlement's capacities. 35 pieces of cow and its progeny can be found on the settlement currently. The increase of the cow numbers to 50 pieces is included in the strategic aims of the immediate future. The increase of the dairy-farm's income producing ability and the foundation of a milk processing firm are strategy aims. This latter would serve the satisfaction of the local population claims happening through own business. Above this, a continuous claim would come forward for the milk and dairy products from the single institutions (kindergarten, school canteen, the home of aged ones, local food store, etc.). The creation of the conditions of the milk processing firm and the own realization would happen after the running-in of the cow numbers, so the investment is beginning in the 3. year according to the plan. The planned investment cost 60 000 thousand Ft this year and 60 000 thousand Ft in the fourth year too.

The proprietors asked you – as the employees of CLEVERS Ltd dealing with expert advice and application writing - onto the completion of the business plan. The completion of MODEL Ltd business plan appears as a planning task so in accordance with the strategic aims. The 1. and the 2. tables contain the main relevant data of the Ltd. We leave the

calculation with the VAT out of consideration at the development of the business plan. We disregard the planning of the by products – straw, organic fertiliser – because a biogas entrepreneur – according to the conditions fixed in contraction – directs it for the Ltd. So to these products we do not order yields and we do not plan with the related expenditures in the case of the organic fertiliser.

The development of the first year of the plan happens on the practical lessons, beside teacher management. We use Microsoft Office Excel program algoritmising the process of the plan making at the planning. The explanation of the causal connections of the algorithm can be found in the educational aid containing the description of the algorithm. The plan of the 4.

year is drawn up independently in the framework of team work by the students, and they prepare the complex business plan of the Ltd according to the granted content and formal requirements. They have to hand in the complex plan printed. The exam will be the protection of the business plan. The students need to prepare a presentation and to protect the business plan. That bank specialist will be present at the defence where the Ltd hands in his loan application.

We do not follow the accountancy regulations in all cases punctually at the planning for example the detailing of the expenses, etc. We find it more important that let the causal connections be traceable for the students step by step based on the numbers. To the first year we teach the planning of the important items in detail relevantly.

MODEL Ltd was founded in 15of January 2005. to indeterminate time, and it worked as a pre-company between 15-29 January 2005.

The number of the trade register: Cg.15-o2-305270 The trade register date: 30 of January 2005.

The company's members:

Nagy Benőné (born as Spórolós Lujza) (business share 30%/

Nagy Benő (business share 30%)

jr. Nagy Benő (business share 20%)

jr. Nagy Benőné (born as Okos Piroska) (business share 20%)

The company's main scope of activity: Agricultural activity – cultivation, and animal husbandry, agricultural service.

The company guides double entry bookkeeping, prepares annual report, it is a subject for the corporation tax and the VAT.

The company can show its business result equally with a total cost and flow costly procedure based on the accountancy law, it developed its account order and book- keeping according to this.

It establishes the profit or loss (P&L) by total costs method according to a variant

“A” in his annual report (but it can establish its P&L by both of the total costs and turnover costs method). It makes annual report from the calendar year with a 31 of December reporting date. The business year is equal to the calendar year.

The assessment sets out from the principle of the continuation of the commerce adequately according to Sz Tv the 14. §, so it applies the actual getting in and production value consistently.

Applied valuation methods:

Fixed assets:

can be founded in net value in the balance sheet Current assets:

Inventories are assessed at actual purchase price.

The assessment of the self-manufactured stocks happens at direct average production cost.

The trade debtors are featured at the sum acknowledged by the customers.

The other receivables are featured in the balance sheet appreciated individual wise at a whole amount.

The liquid assets are featured according to the bank account statements and petycash in the balance sheet.

Liabilities:

The subscribed capital is featured similarly with the deed of association and the registry court entry.

The profit after taxes of the previous years and the P&L for the year get into the accumulated profit reserve based on the member's meeting's decision.

The received state support not to be refunded gets into a capital reserve.

The suppliers are featured at a sum acknowledged by the Ltd individual wise.

The assessment of the other short term liabilities happens similarly to the suppliers.

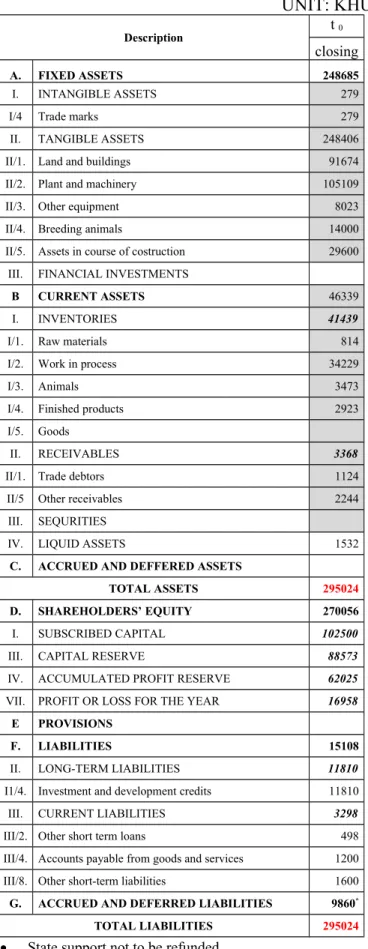

The company amortizes the tangible assets under 100 thousand Ft of unique procurement price in one sum at installation. It reckons with residual value at the calculation of amortization. Tables 1.; 2.; 3.;4. and the 5. contain the status data relevant to MODEL Ltd.

TASK: Fill the absent data of the closing balance sheet based on the data standing for the provision, and open the starting balance sheet of the plan year. (It is necessary to fill the absent data of the table 1. with the status data and with the data of the table 2. and in 3.

standing for the provision.) After that it is necessary to open the balance sheet of the first plan year, which it is necessary to use for the planning. This balance sheet will be the table 57. of the financial plan part.

Table 1. The balance sheet of MODEL Ltd UNIT: KHUF

Description t 0

closing

A. FIXED ASSETS 248685

I. INTANGIBLE ASSETS 279

I/4 Trade marks 279

II. TANGIBLE ASSETS 248406

II/1. Land and buildings 91674

II/2. Plant and machinery 105109

II/3. Other equipment 8023

II/4. Breeding animals 14000

II/5. Assets in course of costruction 29600 III. FINANCIAL INVESTMENTS

B CURRENT ASSETS 46339

I. INVENTORIES 41439

I/1. Raw materials 814

I/2. Work in process 34229

I/3. Animals 3473

I/4. Finished products 2923

I/5. Goods

II. RECEIVABLES 3368

II/1. Trade debtors 1124

II/5 Other receivables 2244

III. SEQURITIES

IV. LIQUID ASSETS 1532

C. ACCRUED AND DEFFERED ASSETS

TOTAL ASSETS 295024

D. SHAREHOLDERS’ EQUITY 270056

I. SUBSCRIBED CAPITAL 102500

III. CAPITAL RESERVE 88573

IV. ACCUMULATED PROFIT RESERVE 62025

VII. PROFIT OR LOSS FOR THE YEAR 16958

E PROVISIONS

F. LIABILITIES 15108

II. LONG-TERM LIABILITIES 11810

I1/4. Investment and development credits 11810

III. CURRENT LIABILITIES 3298

III/2. Other short term loans 498

III/4. Accounts payable from goods and services 1200

III/8. Other short-term liabilities 1600

G. ACCRUED AND DEFERRED LIABILITIES 9860*

Table 2. The structure of missing items of closing balance sheet

Description Unit Unit price

(HUF/t, kg) Amount Stock value (KHUF)

Planned time

period Remark Finished products (own production)

Silage t 8000 365 2920 290 days Permanently

bonded Purchased products

Hay t 7000 59 413 180 days

Permanently bonded

Grains t 20000 1,45 29 7 days Safety supply

level

Milk replacer kg 210 137 29 10 days Safety supply

level

Calf Starter kg 160 192 31 10 days Safety supply

level

Milking complete kg 130 2082 271 10 days Safety supply

level

Total 773

Other materials Animal health materials KHUF/day

1 10 10 days Safety supply

level

Other materials KHUF/day 3 30 10 days Safety supply

level

Total 40

TOTAL MATERIALS 813

Opening receivables Trade debtors (the sales

revenues of milk) KHUF 1124

Milk quota KHUF

231 Gas oil excise tax KHUF

1157 Other receivables KHUF

856 Total other receivables KHUF

2244

TOTAL RECEIVABLES KHUF

3368 Opening liabilities

Accounts payable KHUF

1200 Other short-term

liabilities (STL) KHUF

1600 TOTAL SHORT-

TERM LIABILITIES 2800

Table 3. The structure of fixed assets of MODEL Ltd

Description

Central administration Cultivation Precision technique

Capitalized value (KHUF)

Residual value (KHUF)

DEP base

(KHUF) % Net value(KHUF)

Capitalized value (KHUF)

Residual value (KHUF)

DEP base

(KHUF) % Net value(KHUF)

Capitalized value (KHUF)

Residual value (KHUF)

DEP base

(KHUF) % Net value(KHUF)

Intangible assets 417 0 417 33 279

Land, buildings 6470 647 5823 3 5500 4941 494 4447 3 4200 0

Plant and

machinery 1280 246 1034 10 971 66850 13370 53480 14 44389

Vehicles 10370 2074 8296 20 7052

Investment

(Machines) 27600 5520 22080 1

4 Investment

(Building) 2000 200 1800 4 0

TOTAL 18537 2967 15570 13802 71791 13864 57927 48589 29600 5720 23880

Ancillary plant Milk production dairy-farm

Plant and

machinery 50936 5094 45842 3 43296 40500 4050 36450 2,5 38678

Vehicles 76280 15256 61024 14 59194 27000 5400 21600 14 20952

TOTAL 127216 20350 106866 102490 27000 9450 58050 59630

DEP: depreciation

Table 4. The establishment of the plant order

The table Plan year-1 Plan year-2 Plan year-3 Plan year-4

sign ha Spring Next year Spring Next year Spring Next year Spring Next year

Z-1 5

Corn Wheat Wheat Maize for

silage

Maize for

silage Wheat Wheat Rape

Z-2* 27 Rape Wheat Wheat Rape Rape Wheat Wheat Rape

Z-3 30 Wheat Maize Maize Wheat Wheat Maize Maize Wheat

Z-4 13

Wheat Maize Maize Wheat Wheat Maize for

silage

Maize for

silage Wheat

Z-5 33 Wheat Maize Maize Wheat Wheat Rape Rape Wheat

Z-6 10 Wheat Maize Maize a Maize for

silage Maize for

silage Wheat Wheat Maize

Z-7 27 Wheat Rape Rape Wheat Wheat Maize Maize Wheat

Z-8 116 Maize Wheat Wheat Maize Maize Wheat Wheat Maize

Z-9 29 Wheat Maize Maize Wheat Wheat Maize Maize Wheat

Z-10 6 Rape Wheat Wheat Maize Maize Wheat Wheat Wheat

Z-11 5 Maize for

silage Maize Maize Wheat Wheat Maize for

silage

Maize for

silage Wheat

Z-12 7 Maize for

silage There is not a tenancy agreement

Z-13 14

Maize Maize for silage

Maize for

silage Wheat Wheat Maize Maize Maize for

silage

Total 322

*The boards coloured with green get wedged in Sárgarigó Nemzeti Park, because of this agro-environmental program concerns onto these 262 ha boards.

Table 5. The establishment of sowing

Description Plan year-1 Plan year-2 Plan year-3 Plan year-4

Spring Next year Spring Next year Spring Next year Spring Next year

Wheat 142 154 154 151 151 164 164 143

Maize 135 120 120 122 122 100 100 126

Maize for silage 12 14 14 15 15 18 18 14

Rape 33 27 27 27 27 33 33 32

Total 322 315 315 315 315 315 315 315

3.2 The making of the sales plan

The content dissection serves the aim that the plan making process, the causal connections between the single plan parts and the obligatory number identities is to be traceable. It occurs often that the completion of the single plan parts is needed to happen in parallel with each other since the single plan parts are founded on each other, that is the observed content, rigid separation is not possible in the course of the practical planning work. All this means that it is necessary to draw up the single plan parts in parallel with each other in many cases, and the order of the previously sketched content elements of the business plan concerns its content construction, but it is out of mesh with the process of the plan making. Above this the peculiarities of the agriculture give reasons to the change of the order of the single plan making tasks as we will see this. It is important to underline that the planning period is a year onto all of the planning tasks. A month is the unit of the dissection of the planning period. It is needed to handle as an important aspect, that let the the dismolition of the expenditures, the expenses and the result statement be in accordance with the accountancy politics and accounting system of the company at the single plan tasks. The sales plan means the planning of the volume of the products and services getting to the realization. The Ltd sales plan covers the undermentioned areas based on the sketched strategies:

plant protection service;

the cultivation;

the milk production dairy-farm.

The sales plan of the plant protection service: the making of the sales plan means a combined task in the case of this service, because includes the pricing too. It follows that we will have an opportunity to draw up the sales plan of the plant protection service after the accomplishment of more related planning tasks only. We are talking about the service, so the sales plan and the production plan overlap each other. As a first step so – built upon the basic data of table 6. and 7. – we have an opportunity to define the volume of the contracted service. So the definition of the volume of the service (its cumulative area) and the pesticide need by types appear as planning tasks – in this latter case we disregard the planning according to the pesticide types for the aim of the simplification and we reckon with the specific pesticide expense in pesticide type group dismolition. The cumulative area gives the volume of the realization.

Cumulative area = sowing area * the number of treatments

TASK: Since it is necessary to convince the source giver about the benefits of the application of the precision technologies and the condition system of its introduction, etc. based on literary sources and their related studies, sketch the advantages and disadvantages of the application of the precision technologies (artificial fertilizer, plant protection sowing, etc.), the condition system of the conversion and its financial projections in team work. /The task is needed to be solved independently in a team work. /This task is an important part of the business plan (product chain analysis, it connects to the marketing part functionally).

The teams give a lecture and they report on their received results, in the framework of practical lessons. The single teams value each other’s work/. The relevant informations about the Ltd are used at the solution.

TABLE 6. THE AREA TO BE HANDLED AND THE NUMBER OF THE TREATMENTS

Description III. IV. V. VI. VII. Total

plant ha month treatment ha

Wheat 250 1 1 2 4 1000

Autumn barley 150 1 1 2 300

Maize 500 1 1 1 3 1500

Sunflower 250 1 1 250

Total 1150 1 3 4 2 10 3050

SOLUTION:

Table 7. The partition of the cumulative area

Description Area

(ha)

III. IV. V. VI. VII. Total

ha (ha)

Wheat 250 250 250 500 1000

Autumn barley 150 150 150 300

Maize 500 500 500 500 1500

Sunflower 250 250 250

Total 1150 500 900 1150 500 3050

The sales plan so means the plant protection service of 3050 ha cumulative area.

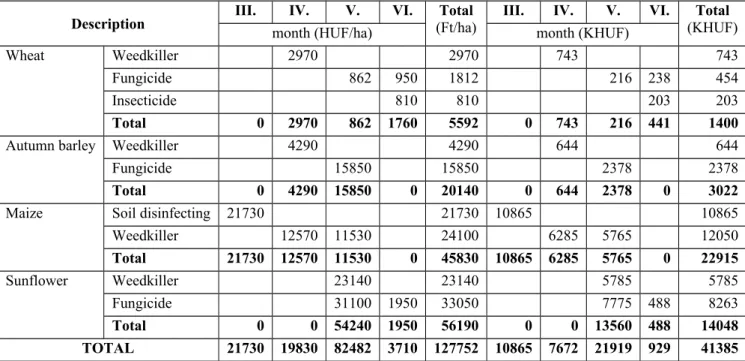

Table 8. The establishment of the expense of the specific pesticide

Description III. IV. V. VI. Total

(Ft/ha) III. IV. V. VI. Total (KHUF)

month (HUF/ha) month (KHUF)

Wheat Weedkiller 2970 2970 743 743

Fungicide 862 950 1812 216 238 454

Insecticide 810 810 203 203

Total 0 2970 862 1760 5592 0 743 216 441 1400

Autumn barley Weedkiller 4290 4290 644 644

Fungicide 15850 15850 2378 2378

Total 0 4290 15850 0 20140 0 644 2378 0 3022

Maize Soil disinfecting 21730 21730 10865 10865

Weedkiller 12570 11530 24100 6285 5765 12050

Total 21730 12570 11530 0 45830 10865 6285 5765 0 22915

Sunflower Weedkiller 23140 23140 5785 5785

Fungicide 31100 1950 33050 7775 488 8263

Total 0 0 54240 1950 56190 0 0 13560 488 14048

TOTAL 21730 19830 82482 3710 127752 10865 7672 21919 929 41385

The Ltd plans the realization of 41 385 thousand Ft pesticide in the framework of the plant protection service.

The sales plan of the cultivation: the sales plan of the cultivation plannable only in the knowledge of the sowing structure. The sowing structure can be developed only in the knowledge of the tillage area demand of the fodder supply of the animal husbandry. This area will be identical with the area demand of the necessary own produced fodder quantity. We can concretize the necessary fodder in the knowledge of the number of the forage days and the content of the fodder portions only on the other hand. It is possible to plan the number of the forage days based on the livestock change plans only. The context of concretizing the tillage area:

Maize for silage demand (t)= 1-lossSilage%(in demandfactor form)

The area of maize for silage (ha) = Maizeforyieldsilage(t/ha)demand(t)

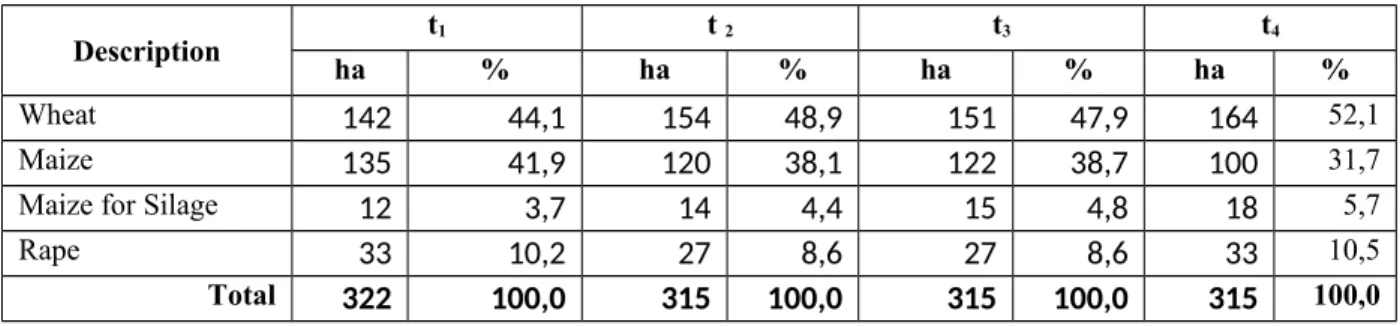

The algorithm of the related planning task can be found in the educational aid of The algorithm of the business plan. Based on the results received there, the area demand of the first yearly silage need of the dairy-farm is 14 ha, so it is necessary to sow silo maize on an area of this size. Based on the data standing for the provision, the sowing structure exfoliates according to table 9. regarding to the planning period relevantly. (It is important to accentuate, that the planned area differs or can deffer from the area size covering the fodder need concretized punctually because of the table measure.)

Table 9. The main data concerning the sowing structure

Description t1 t 2 t3 t4

ha % ha % ha % ha %

Wheat 142 44,1 154 48,9 151 47,9 164 52,1

Maize 135 41,9 120 38,1 122 38,7 100 31,7

Maize for Silage 12 3,7 14 4,4 15 4,8 18 5,7

Rape 33 10,2 27 8,6 27 8,6 33 10,5

Total 322 100,0 315 100,0 315 100,0 315 100,0

As this is visible based on the data of the table 4., the owner of Z12 board did not extend the tenancy agreement with the Ltd. The size of plough-land decreased with 7 ha because of this.

The 315 ha area is the property of the owners of the Ltd. Taking the planned yields as a starting point in the knowledge of the sowing structure – the planned average yields are the following: wheat: 6,2 t/ha, maize: 8,2 t/ha, rape: 3,3 t/ha, silo maize 37,5 t/ha - the sales plan of the Ltd. develops according to the table 10.

Table 10. The sales plan of the cultivation of the Ltd.

Name VIII. X.

Total /ton/

month

Wheat 880 880

The milk production dairy-farm's sales plan: the dairy-farm's sales plan can be prepared likewise only based on the production plan of the section that is the knowledge of the livestock change. The related basic data are the undermentioned ones onto the dairy-farm:

The period passed between two calvings:

410 days

Average milk production: 7000 litres/lactation

The newborn calves (bull-calves) are got to realization with live weight of 65 kg/pieces.

The culled cows are got to realization as a beef cattle with live weight of 600 kg/pieces.

The sales volumes concerning the meat will be identical with values in the livestock change plan. To concretizing the sales volume of the milk it is needed to know the milk yield calculated for a year. We can concretize this so if we correct the passed time between the two deliveries onto a year. We can do the correction with proportioning based on the algorithm which can be observed on the figure 2.

Figure 2.Concretizing the yearly average milk production 410 days

lactation period dry period

350 days (85,4%) 60 days(14,9%)

365

lactation period dry period

365*0,854= 312 days 365-312=53 days

Yearly average milk yield(l/pieces)

7000 litres:350 days = 20 litres *312 days = 6240 litres/year

The volume data of the plan year realization of the dairy-farm develop according to the data in the table 11. The average numbers of the plan year is 37 pieces, all of the milk yield is so 37*6240=230880 litres. At the planning of the dairy-farm's yearly yield it is necessary to take into consideration the period establishment of the yield as an important viewpoint primarily at the establishment of the milk yields, in spite of the fact that there is not changing in the combination of the fodder portions and the animals get the same fodder all year. In the practice the winter and the summer yields develop differently. Above this the establishment of the deliveries in time – the milk production of cows gave birth in the initial period of the perzistencia is taller – has an effect on the yield. The practical factual figures are the normative ones at the planning of the meat output likewise. We accept it despite all these – because of the simplification – the sales data in the table 11.

3.3 The content and the making of the production plan

The producer companies have to plan the company's production tasks beside the sales plan.

The planning of the production task means the planning of all of the given yearly output /yield/ of the company planning in natural, in unit measurement and in money value. The consideration happening in the natural unit of measure is necessary in order that we define the value of the supply calculated on a direct average production cost.

Table 11. The sales plan of the dairy-farm

The calculated measure is needed at the partition of the ancillary plant's expenses, for example the ancillary plant’s economy technique index-numbers - shift clock, shift day, nha, tkm, etc. Obvious, that there is a very tight contact between the sales plan and the production plan. The two plans are not necessary to be the same despite of this. It can have some reasons:

The two activities – that is the production and realization – differs or can differ in time from each other. Because of this in the given year the volume of the sold products can be more or less, than the output of the production activity of the given year (for example the product, which was produced in the previous year so this is a product on a supply, is got to realization in the object year).

The inevitable concomitant of the product production /the insurance of continuous production/ is that work in progress, intermediate and semi-finished products are issued in the case of a given production process.

The company can produce onto a supply based on his commercial politics or can accomplish own investment made in own company, etc.

Month Milk Calf Culled cow

litres kg

I. 19240

II. 19240

III. 19240 260

IV. 19240

V. 19240

VI. 19240 260 1800

VII. 19240

VIII. 19240

IX. 19240 260

X. 19240

XI. 19240

XII. 19240 260 1200

Total 230880 1040 3000

supplies with self-manufactiured stocks and with the stock change of own performance capitalizes. The production plan – in generality - includes the undermentioned items:

Finished products getting to realization

Semi-finished products getting to realization

Services getting to realization

Own performance capitelized

Self-manufactured stocks

A) Work in progress b) Semi-finished products c) Finished products d) Animals

The production plan of the Ltd includes the items written aslant.

The production plan of the plant protection service

In the case of the plant protection service the production plan – considering the volume – is identical with the sales plan. So the cumulative area of the demanded complex plant protection service is 3050 ha. The production plan means the planning of the plant protection technologies of the different vegetal cultures likewise in the case of the service, which includes the undermentioned ones:

the size of the cumulative area in breaking down plants,

the pesticide need for different kinds and plants,

the number of the necessary shift days,

the number of the necessary workdays.

The knowledge of these expenditures constitutes base for the planning of the expenses and the price of the service. Its structuration in time, in accordance with the technologies and the plan of cash flow, has to happen on a monthly level.

The production plan of the cultivation: the production plan of the cultivation includes the expenditures of the object year sowing structure, and the next yearly cultivation (value of cultivation). The knowledge of the sowing structure and the technological plans is the basis of its completion. There is need for the planning of the next yearly cultivation because the expenses as current assets coming forward seasonally, which are emerging in the object year transform to property that is they appear as a supply. It is necessary to see that the expenses activated as the supply do not have an effect on the object year result. We review the process of the completion of the production plans – for the resuscitation of the body of knowledge – taking the wheat as a starting point. The technological basic data of the wheat growing projected to 100 ha can be found in the table 12. and 13. It is necessary to plan the technologies on the field level in the practice because of the different conditions of the given field. Reasonable, that the planned expenditure of the growing technology changes depending on this because the planned yield is defferent, the quantity of artificial fertiliser, the forecrop differs, etc. Based on the data in the table it is verifiable, that the undermentioned expenditures get to planning in the technology plan in chronological order:

the work processes,

the yield,

the material needs (artificial fertiliser, pesticide, other materials),

the expenditures of the ancillary services (workday, nha, combine harvester ha, etc.) as power machine categories,

the quantity of the external services,

the direct manual workforce demand.

In the knowledge of the sowing structure (the product of the actual area/100 and the expenditures of 100 ha) can be concretized the total expenditure of the sowing structure of the Ltd. In the knowledge of this – taking all of the necessary shift days as a starting point - can be planned the expenditures of the assistant firm services and the expense places of the cultivation (the general expenses of cultivation).

The production plan of ancillary services

The plant protection service and the mechanical work demand of the cultivation provide the basis of the production plan of the ancillary services. The concretizing of this happens with the summing up of the mechanical work demand coming up in the technological plans, according to the category of the power machines. We use economy technique index-numbers for the consideration of the need, pl. normalhectare, combine hectare, shift day, etc. In the case of the Ltd we plan with shift day. The partition of the ancillary plant expenses to the cost bearers happens according to the shift day.

The basis of dairy-farm's production plan is the livestock change plan. This includes the change in number of the livestock (for example progeny, external and internal changes, etc.), the weight gain, and live weight planning, the planning of the number of the forage days according to age groups. The efficiency indicators were the undermentioned ones at the completion of the dairy-farm's livestock change plan:

time passed between the two calvings is 410 days,

falling out (death, involuntary slaughter) o newborn calf: 5 %

o weaned calf 3%

o heifer (yearling) age group 2%

o replacement heifer age group 1%

the weaned calf gets to realization (the time frame of the age group: 0-80 days, weight limit: 40-65 kg)

culled cow is 15%

fertile index is 1,5

the planned milk production (6675 litres/piece/year)

milk quota is 189000 litres/year